3 Intangible Assets Best to Maximize in IP Transactions

Introduction: Unlocking Value from What You Can’t See

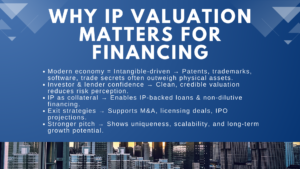

Turnover of intangible assets such as, and not limited to, intellectual property (IP), brand equity, software, and customer relationships with consumers are considered more valuable than tangible assets in the current knowledge driven economy. You can make or break a business buy, rent and sale by simply knowing how to locate, place in line with value and form of these intangible assets. This is more so in sectors such as tech, media and in the medical field where innovation and brand name are the major driving forces in long term profitability.

Nevertheless, most companies undervalue or mismanage these assets in negotiations and this leads to losing out bargains of improving tax, values, or of obtaining strategic positioning. We will segment the value maximization of intangible assets relating to IP transactions in this paper in planning early on, and integration after the deal has been concluded.

Understand the Types of Intangible Assets Involved

Not every an intangible is the same-nor all of them are on the balance sheet. Some common types include:

Intellectual Property (IP): Copyrights, patent, trade secrets, trademarks.

Contractual Rights: franchise, licensing, and customer contracts.

Intangibles connected with the brand of goods: Brand loyalty, domain names, reputation.

Technology & Software: Code, platforms, algorithm, proprietary.

Human Capital/ Know-how: Key personnel pacts, knowledge, processes.

Always carry out a substantial audit of all intangible property, such as off-balance-sheet IP, before entering any particular transaction. Recording and classifying these assets early may enhance due diligence, bargaining strength and valuation.

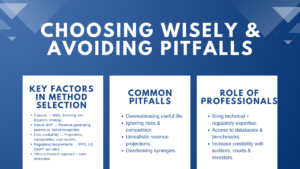

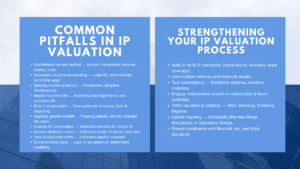

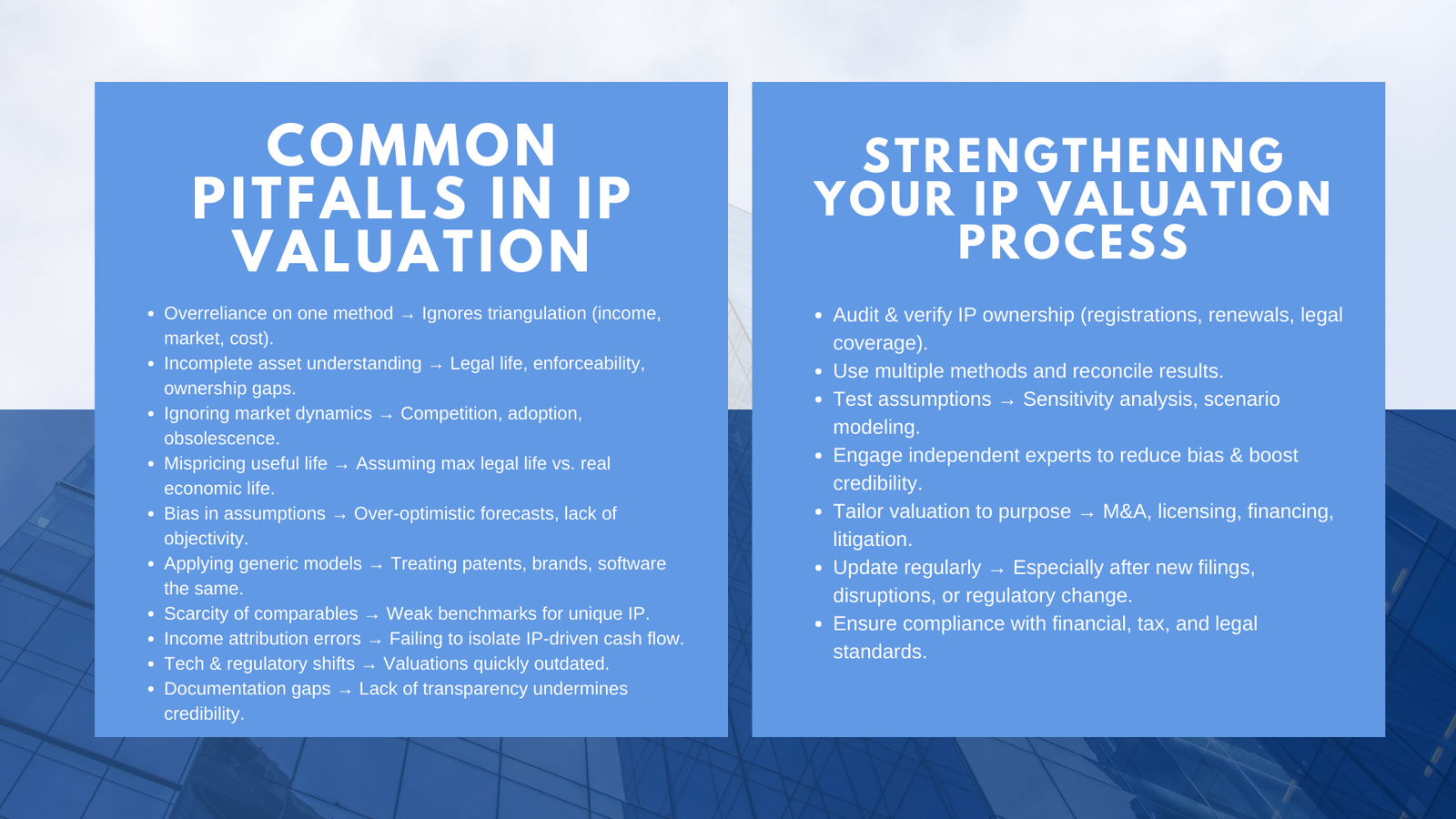

Conduct a Proper Valuation Using Accepted Methods

Appraisal is one of the steps that are very fundamental in an IP transaction. The most popular ones are:

Income Approach: Comes up with the estimate that is based on future income that the IP would generate (e.g., discounted cash flow).

Market Approach: Comparisons in the market on similar transactions in IP.

Cost Approach: Determines the estimated cost of the recreation or replacement of the asset.

Both of them possess their advantages depending on the character of the IP and accessible information. An example is a software startup where SaaS is recurring and a software start up would develop better with an income approach attracting any market basis than the brand names that would figure better with a market-based benchmark.

Ensure that your valuations are documented and defendable particularly in respect to regulatory, tax and audit.

Align IP Allocation with Strategic Goals

The way you impair valuing intangible assets will affect your tax, ROI and deal flexibility. For example:

Particularly, buyers could prefer more value on amortizability intangibles (e.g., contracts, technology) in order to obtain more future tax deductions.

The sellers might like to enjoy a capital gains treatment by selling to goodwill or brand.

In cross-border transactions, the jurisdictional effect of the transfer pricing and withholding tax on IP value are to consider.

Strategic IP allocation is not only a tax issue but it has everything to do with the fit of your financial decision structure to your future growth plans or integration of the asset.

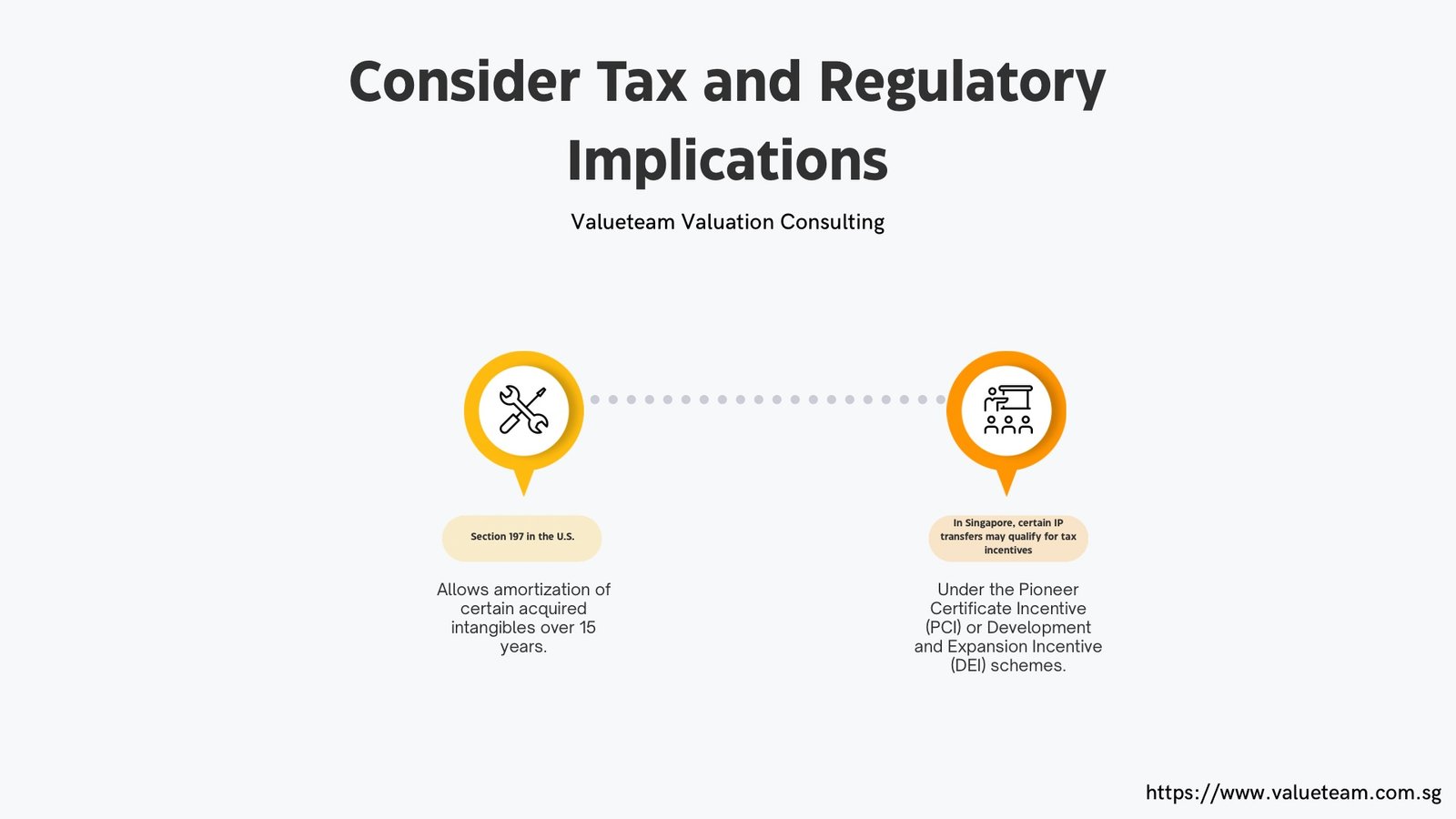

Consider Tax and Regulatory Implications

The taxation of such intangible assets in jurisdictions such as Singapore or U.S can vary greatly based on the classification and transfer guidelines.

For example:

The 197 section of the U.S. permits amortization of the acquired intangibles within a 15 year span.

Some of these IP transfer may be tax-incentivised by the Pioneer Certificate Incentive (PCI), or the Development and Expansion Incentive (DEI) in Singapore.

Caution is also not to be forgotten in evaluating rules of transfer pricing in intra-group efforts of transferring IP, more so to down-tax jurisdiction. Following cooperation with international tax advisors can guarantee adherence to compliance and assist in unwanted tax exposure.

Strengthen Legal Protection and Documentation

intangible assets valuation methods can be valued based on what is possessed as well as how adequately this is being guarded. As close to the transaction process please ensure:

All the IP rights are clearly assigned and registered (patents, trademarks, software codes).

Delivery is transferable and enforcible in case of license and usage rights.

It has no under encumbrances or third party claims.

Register elaborate figures and guarantees in sale or licensure

put on pacts. Once there are any loopholes on IP protection or ownership this will devalue and may postpone deal by more than eight days or even annul the entire deal.

Post-Transaction Integration and Monitoring

These are the post-transaction integration and monitoring.

After the transaction will be closed, there will be no end of your job. Particularly to acquirers, value creation is reliant upon how properly you incorporate the intangible assets in your practice.

This includes:

Installation of purchased IP in product or marketing strategies.

Aligning and retaining talent associated with the IP.

To keeps on protecting, sustaining or creating the IP portfolio.

Calculating ROI and making business adjustments.

Certain companies also perform IP audits on a periodical basis after a deal in order to know whether they are on track as per their strategic objectives and to be aware of the risks or opportunities in the market.

Conclusion: Turning Intangibles into Strategic Assets

The key to maximizing intangibles in IP transactions is not to make entries in the accounts but to make long-term value unlocked. The treatment of your intangibles may greatly impact financial and operating results whether you are a buyer aiming at future development, a seller trying to achieve the best exit mark or a business handling deals of licensing.

Through the identification of all the important intangible resources, employment of sensible valuation strategies, designing tax-intelligent allocations, and defending rights through legal means, you are transforming intangible value into real business benefit. Waiting until due diligence to do so means that you should start managing your IP portfolio as an asset today.