Certified IP Valuation Methods Training Singapore

Common IP Valuation Approaches: Cost, Market, and Income Methods

Introduction to Certified IP Valuation Methods Training Singapore

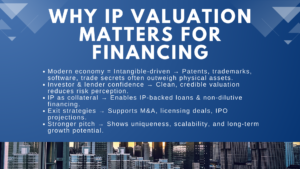

Intellectual property (IP), in the modern economy, has become one of the most precious categories of intellectual property valuation methods for M&A. IP, whether as patents, trademarks, software, proprietary technology or otherwise, can typically represent a significant fraction of the enterprise value of a company. Unlike physical assets, intellectual property does not have a tangible form that can be easily valued based on historical cost alone. Its value is intrinsically tied to future economic benefits, market position, and legal protections.However, as opposed to the property of an inanimate nature, intellectual possessions cannot be valued by simple historical costs. Rather, fair value is determined by professional valuation specialists who use well-developed approaches based often on international standards e.g. IFRS 13 (Fair Value Measurement) or the International Valuation Standards ( IVS 210 -Intangible Assets ). There are three most popular methods of valuing IP which are Cost Approach, Market Approach and Income Approach. All of these approaches offer another prism at the ways in which the economic value of intangible assets can be approached.1. The Cost Approach: Measuring Investment and Reproduction

The Cost Approach measures the worth of IP, using the cost that would be incurred in order to recreate/reorganize or substitute the asset at its current utility. It is a fine approach to use in cases where the IP is not old and in cases where similar market data does not exist. There are two variants that are normally applied:- Reproduction Cost Method: calculates the cost that is required to reproduce a perfect copy of the existing IP.

- Replacement Cost Method: Determines the amount it would cost to make an asset with the same utility which is functionally similar.

2. The Market Approach: Using Comparable Transactions

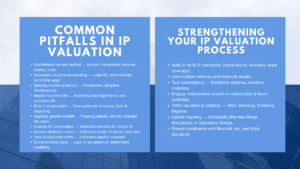

Approach of the Market identifies value based on the subject IP being compared with similar property which has been bought, licensed or otherwise transacted within the market place. It resembles conceptually fixed analysis of real estate or business. The implied multiples or royalty rates are based on royalty rate database, licensing standards and even published transactions. They are adjusted when there is variation in the market potential, exclusivity, geographical scope and risk. Indicatively, a pharmaceutical firm that highly regards a patent to a new drug may be using licensing dealings on comparable drugs to set a suitable market-based royalty payment. This approach is however difficult to do in practice since access to the useful comparable data is often restricted because IP transactions are quite confidential. Example: A pharmaceutical company valuing a patent for a new drug may examine royalty rates and transaction prices of comparable drugs in the same therapeutic area. The observed rates are then adjusted to account for the drug’s uniqueness, patent life, and market potential. Challenges: The market approach is often limited by the availability and confidentiality of transaction data. Many IP deals are private, making it difficult to obtain reliable comparables. Despite this, the market approach provides a market-based benchmark that can be used to cross-check other valuation methods.3. The Income Approach: Quantifying Future Economic Benefits

Income Approach is the most common and theoretically sound approach towards IP valuation. It quantifies the worth using the present value of economic benefits likely to be made in the future using the asset. Typical means of income-based methods are: Relief-from-Royalty (RFR): The amount of value estimated as undefined by the royalties that a company would have to make in case the IP is not owned. Excess Earnings Method: The excess profits are charged to the IP, and such excess profit is determined after excluding the gains on the tangible and other intangible assets. Incremental Cash Flow Method: The incremental cash flows can be quantified as the cash flows which can be traced to the ownership or the use of the IP. The risk profile of the IP and market is manifested in the chosen discount rate. This method is much more common in financial reporting, M&A deals and litigation support. The chosen discount rate reflects the risk profile of the IP and the market environment, ensuring that the valuation accounts for uncertainty and the potential variability of future benefits.Conclusion

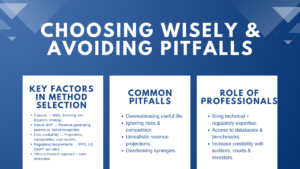

The appropriate method of valuation will be determined by the purpose, how to value intangible assets for financial reporting, the availability of information and the developmental level of IP. The Cost Approach is applicable with initial-stage R&D assets, the Market Approach would fit with the benchmarks of the licensing, and the Income Approach assists in delivering an in-depth look at the potential of the income generation. Practically, professional valuers tend to use several procedures in cross-checking their outcome to achieve defensibility. With the rise of intangibles taking over the balance sheets of corporations, it would be very critical to learn how to work around these valuation models in order to unlock the true value of innovation to investors, auditors, and executives. Accurate IP valuation not only enhances financial transparency but also informs strategic decisions such as licensing, mergers, acquisitions, and litigation planning. Companies that master these approaches are better positioned to maximize the value of their intellectual property and capture competitive advantage in knowledge-driven markets.Frequently Asked Questions

Q1. What is Certified IP Valuation Methods Training?

Certified IP Valuation Methods Training is a professional program that teaches participants how to assess the value of intellectual property assets using recognized valuation methodologies. The training typically covers patents, trademarks, copyrights, software, trade secrets, and other intangible assets used in business, finance, and investment decisions.

Q2. What are the main IP valuation methods covered in the training?

Most IP valuation courses focus on the three primary valuation approaches: the Income Approach, Market Approach, and Cost Approach. Participants learn when each method should be applied, the advantages and limitations of each approach, and how valuation professionals select the most appropriate methodology for different situations.

Q3. Who should attend IP valuation methods training?

The training is valuable for valuation analysts, accountants, auditors, finance professionals, intellectual property managers, consultants, lawyers, investors, business owners, and corporate executives who need to understand the financial value of intangible assets and intellectual property.

Q4. Why is understanding IP valuation methods important?

A strong understanding of IP valuation methods helps organizations make informed decisions regarding licensing, fundraising, mergers and acquisitions, financial reporting, tax planning, litigation support, and strategic asset management. Accurate valuation can also improve transparency and support negotiations with investors, buyers, and business partners.

Q5. How are IP valuation methods applied in real-world situations?

Valuation professionals often apply one or more valuation approaches depending on the purpose of the engagement, the type of intellectual property involved, and the availability of reliable data. In practice, multiple methods may be used together to validate results and produce a more robust and defensible valuation conclusion.