IP Valuation for Financial Reporting and Audit Compliance

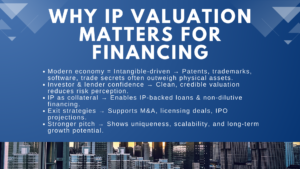

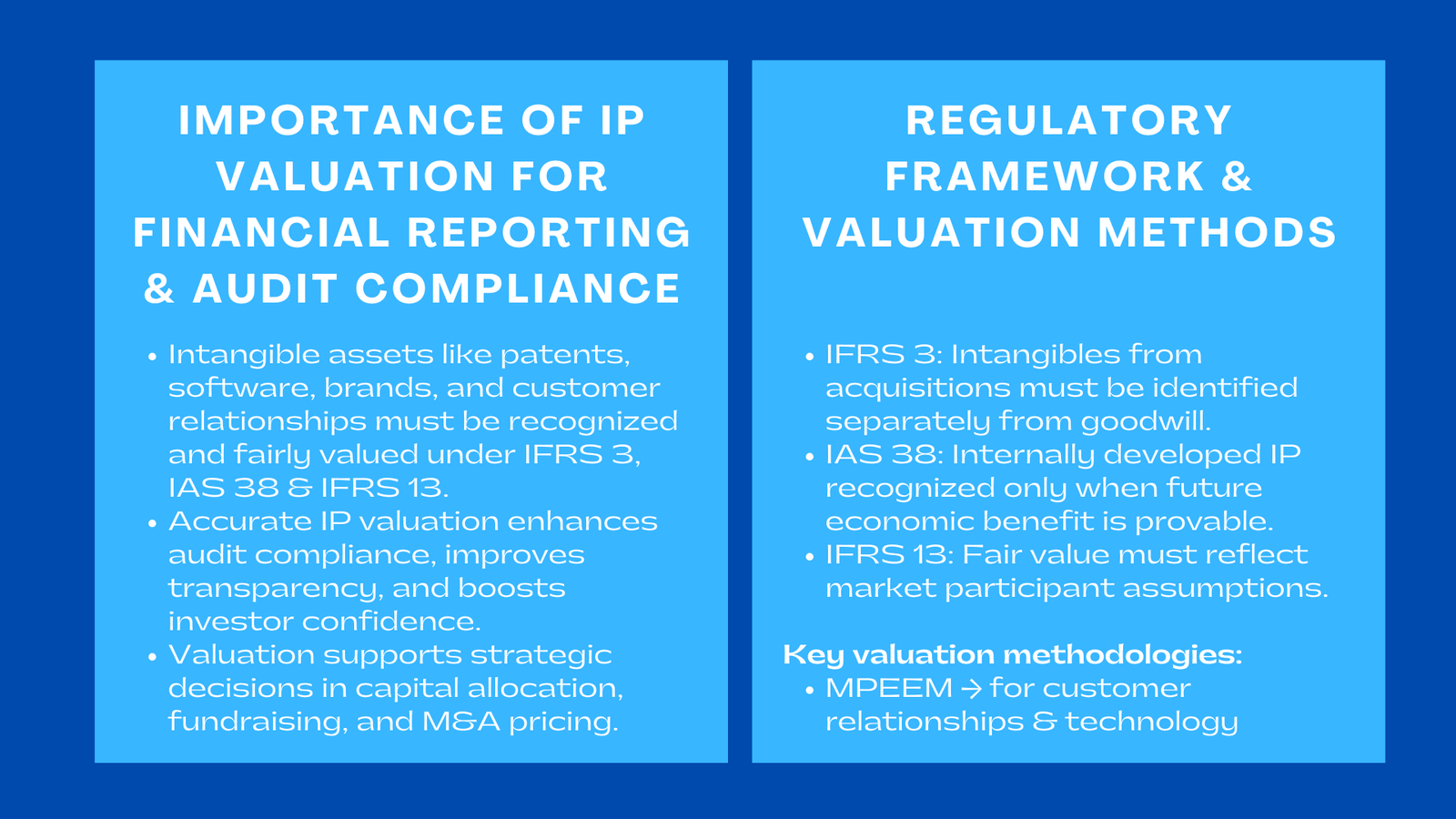

In the era of knowledge-based economies, intellectual property has stopped being an off-balance-sheet item. International accounting standards (IFRS 3, IAS 38 and IFRS 13) call for identifiable intangible assets like patents, brands, software and customer relationships to be recognised and measured to fair value in financial statements.

Proper IP valuation leads to audit compliance, transparency and investor confidence. The true economic position of companies can be reflected by accurately measuring these assets and supporting strategic decisioning, as well as showcase the value of innovation to stakeholders. For example, the identification of a patent or proprietary software at fair value can impact capital allocation, investment decisions and merger or acquisition pricing.

However, IP valuation may only be conducted with specialized technical expertise, as it demands science, the field knowledge of how finances work, as well as understanding the legal validity and the particular industries or markets. The appraisers should integrate market data, cost estimates and expected cash flows by considering risk, technological obsolescence and competitive factors. Focusing on globally recognized frameworks of reporting for the valuation activity makes valuations not only correct, but also easily defendable in the event of an audit, regulatory review, or investor due diligence.

In addition to compliance purposes, a strong IP valuation process can deliver strategic value. Companies are able to better understand which intangible assets are creating the most value to make informed decisions for R&D prioritization, licensing, and portfolio management. It adds rigor to mergers and acquisitions negotiations, aids a fundraising process and boosts credibility with investors and analysts.

Ultimately, the part of intellectual property valuation for financial reporting compliance Singapore recognition and value commoditization changes intangibles hop into tangible strategic assets. By following international accounting standards and following strict valuation approaches organizations can ensure that they are maximizing the economic potential of their IP, increasing stakeholder confidence and where possible asserting long term competitive advantage in ever more innovation-driven markets.

Regulatory Context

Under IFR 3 (Business Combinations), Company is required to recognise separately identifiable intangible asset acquired in mergers that ensures its value is accounted for separately from goodwill. This differentiation leads to more accurate financial reporting and gives a true representation of the resources that created the value of such an acquisition to the stakeholders. Proper identification and valuation of such assets also make it easier to amortize them, to test them for impairment and to make strategic decisions after acquiring them, especially when applying IP valuation methods Singapore for financial reporting and audit compliance.

Under IAS 38 (Intangible Assets), the capitalization of internally developed intellectual property is possible if some recognition criteria are met, such as proof of technical feasibility, intention to complete the asset and ability to generate future economic benefits. This makes sure that only those assets will be recorded on the balance sheet that have some measurable and probable future returns and help in maintaining the financial statement reliability and support investment decisions. In other words, the IP value allows firms to annualize the cost within the asset’s useful life to increase the transparency and comparability in financial statement reporting.

IFRS 13 (Fair Value Measurement) provides the framework for ascertaining fair value of these intangible assets using the assumptions of the market participants. This standard focuses on the idea that value should represent the price which would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. Through the implementation of IFRS 13, organizations can be assured that valuation activities are conducted consistently, objectively and transparently as per accountancy practice continues to follow market realities and credible, utilizing information is provided to stakeholders.

Les Capitals taken together provide a holistic model for identifying, measuring and reporting IP. Compliance is not only about ensuring that IP assets are correctly reflected in financial statements, it is also about ensuring IP assets are used strategically when setting investment, acquisition, and operational decisions. Firms that comprehensively use such standards help them prepare for audits, boost investor confidence and maximize the strategic value of their intangible assets.

Valuation Methodologies for Reporting

Relief-from-Royalty Method:

The relief from royalty model is usually used for brands and trademarks. This way, the IP is valued on the basis of its putative future royalties, which would have to be paid under the assumption that the company did not own the asset. By marking up the present value of these royalty payments that would have been paid over time by calculating the economic life of the asset, analysts can measure the financial value gained from ownership. This method is especially helpful for well-known brands or trademarks with comparable licensing transactions available in the market for which a defensible and market-based valuation is provided.

Multi Period Excess Earnings Method (MPEEM):

The Multi-Period Excess Earnings Approach is usually applied in valuing customer relation, core technology, and other intangible assets which produce income indirectly. MPEEM recognizes a share of total estimated profit of the business less returns attributable to other assets that are considered the contributory assets to the asset. This method focuses attention on what portion of the revenue generated can be solely attributed to the IP and, therefore, the economic value of the IP and not on other contributions to the business resources. It is especially relevant to assets which support long-term customer loyalty or proprietary processes that would give an advantage in the competitive environment.

Cost Approach:

The cost approach is used where intellectual property does not have a direct link to revenues, or the future cash flows are uncertain. It can be measured by the cost of the research and development process, labor, materials and implementation of the asset to be able to replicate or substitute the asset. In order to get a realistic valuation, allowance is made for obsolescence, progress in technology and efficiency factors. This approach gives a conservative floor to internally developed assets or assets not generating measurable economic returns as yet.

All approaches to valuation must be carefully documented, including the underlying assumptions. This involves the definition of the economic life of the asset, the choice of suitable discount rates to reflect risk and allowance for contributory asset charges to reflect the returns of other supporting assets. The documentation gives transparency, aids compliance with audit requirements and gives credibility with the presence of documentation in investor communications, M&A negotiations and financial reporting.

By using these valuation methodologies systematically, organizations can measure the economic value of the intangible assets and use them to make informed strategic decisions, optimize licensing and acquisition strategies, and maximize the overall value of an organization. Knowledge management measurement and pricing provides an effective way of converting intangible assets into physical, measurable contributors to the sustained business performance.

Audit Trail and Documentation

Auditors need clear and verifiable evidence in order to make sure that valuations of intellectual property are accurate, reliable and replying to accounting standards. One of the major requirements for the forecasts is source data, consisting of specific financial projections, sales growth assumptions, expense models, and cash flows (underlying the IP). Providing supported forecasts can show that forecast valuations are based on realistic business expectations as opposed to random estimates.

Yet another important factor is the market benchmarks for royalty rates, though other importantly, influencing factors are the legal rules. When using approaches such as the relief-from-royalty approach, auditors are expecting comparables based on licensing agreements, industry standards or third-party transactions. Sometimes these benchmarks are used to check the assumptions that are made in the present value of the future benefits to use them in the valuation procedure to ensure that the valuation will be in accordance with the market reality.

Auditors are also looking for an appropriate reason for a chosen valuation methodology to be justified. Whether applying income-based, cost-based or market-based approaches, organizations will need to discuss why a specific approach is suitable for the type of asset, the economic climate and the specific aspects of the IP audit and IFRS fair value measurement for intangible assets. This rationale is in itself transparent and assists in explaining the professional judgment upon which the valuation is based.

Consistency with the previous financial periods is another critical factor. Auditors evaluate if valuation methods, assumptions and methodologies correspond with previous reporting cycles, or if the changes, if any, are properly accounted for and explained. This ensures that financial statements will have continuity and the ability to compare and this will lead to increased confidence among stakeholders.

Ultimately, good documentation makes the valuation pass the test of an audit. The detailed trails of assumptions, methodologies, market stats, internal approvals not only serve IFRS or local GAAP compliance, but in turn also serve as a defense mechanism if undergoing regulatory reviews, M&A due diligence or investor inquiries. Risks reducedIP valuations are well documented, and create more credibility, reduced risk, and keep intangibles supportive of achieving the organization’s long-term and enterprise goals with greater transparency and confidence.

Conclusion

IP valuation for financial reporting doesn’t have to be a compliance process – it must be a basis for corporate credibility. Accurate and transparent valuations apply to bridge the contrast with innovation and financial recognition. Companies that make the process of valuing IP a governance priority ensure a more trusted environment among investors, improve minority auditor auditing, and prepare them for long-term value creation in a global context.

Moreover, strong IP valuation will provide insights for strategic decision making as it will reveal the intangible assets that contribute most to business value. It allows companies to invest where their money will have the greatest impact, craft licensing deals intelligently and facilitate mergers or acquisitions with defensible financial arguments. By incorporating valuation into corporate governance, organisations turn intangible assets such as intellectual property from ‘an invisible asset’ to a measurable and strategic asset.

Ultimately, the valuation of IP ensures and enshrines both financial integrity and competitive advantage. Organizations who invest in systematic, transparent, and defensible incidence of valuation have been able to not only meet expectations set by authorities but also use their intangible possessions to ensure they are on track for sustainable growth as well as serve as an investment attraction and ensure they maintain control over their position in ever-increasing knowledge-based industries.