Accredited IP Valuation and MA Training

IP Valuation in Mergers and Acquisitions (M&A)

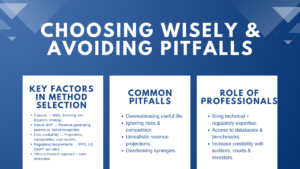

Introduction to Accredited IP Valuation and MA Training

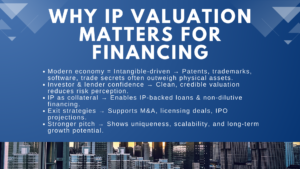

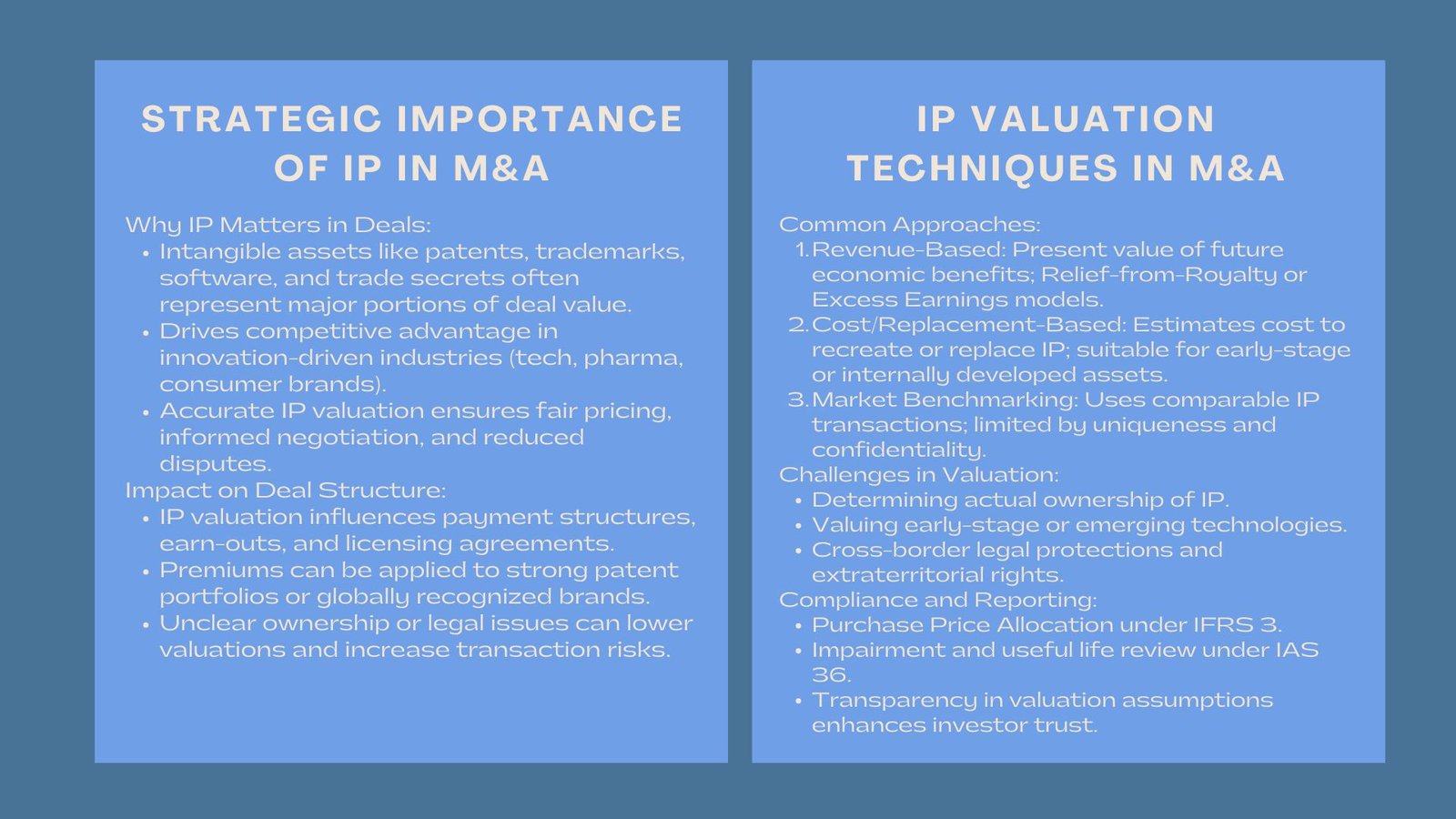

In the contemporary business environment, which is characterized by climax business activities, intellectual property (IP) is becoming a more critical component in determining the success of mergers and acquisitions (M&A). With the emerging industry trends and innovation as the core of corporate development, intangible resources like patents, trademarks, software, and trade secrets tend to present the most significant part of deal value.

However, one of the most complex issues that surround M&A is the value of the intellectual property of a company, one that requires not only accounting skills, but also the knowledge of the market dynamics, technological processes, and legal safeguarding. Even the most promising acquisition may enter into unforeseen risks or financial misrepresentation without any proper IP valuation.

Knowledge on the Strategic weight of IP in Acquisitions.

Why Intellectual Property Determines Competitive Advantage.

Lately, even modern business gets its competitive advantage not in the physical resources, but in innovation and branding. Pharmaceutical firms, consumer brands, as well as technology companies are extensively dependent on their intangible resources to maintain the leadership of the marketplace. This implies that in M&A, a big portion of the acquisition price is dependent on the value of these assets.

Proper IP valuation makes the buyer and the seller aware of the actual functionality of the innovation capabilities. It also averts conflicts and establishes a good base of coming up with fair deals.

Effects of IP on Negotiation and Deal Structure.

In case of the merging of two companies, IP can ascertain the equilibrium of negotiating power. Premium pricing can be charged on a good patent portfolio or a brand that is internationally recognized. On the other hand, ownership or legal issues that go unresolved may reduce valuations and escalate the risk of transaction.

The economic perception of IP held by the buyer has a direct impact on the structure of payments, earn-out, and even the future licensing. Valuation is therefore not a mere accounting activity, it is a strategic exercise that informs the course of the deal.

Techniques of Intellectual Property Value Measurement.

Revenue-Based Estimations

The revenue based method is concerned with the amount of financial gain that the IP will cause in the future. Such techniques as the Relief-from-Royalty, and Excess Earnings models are used to estimate the royalty or profits that a firm would obtain in the case of ownership of the IP. The methods are preferred in M&A transactions as they are in tandem with future economic returns.

This valuation framework is central to IFRS-compliant intellectual property valuation practices for mergers and acquisitions, where financial projections and discount rates reflect fair value assumptions from the perspective of market participants.

Cost and Replacement-Based Assessments.

Others of the IP assets may be best priced estimating the cost of recreation or replacement. It suits well in the case of internally developed technologies or databases that have not been generating revenue but can be of strategic value. Thereafter, obsolescence, development time and opportunity cost will be adjusted.

Market Transactions Benchmarking.

In small industries such as those that deal with licensing and sale of IPs, similar market dealings can be used as a good reference. Nevertheless, intellectual property is hardly the same in every company, and thus it may be difficult to find appropriate comparables. Market benchmarking needs to be professional and have access to credible industry data.

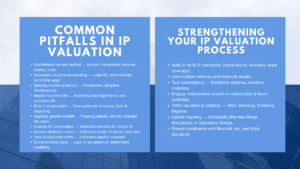

Underestimated Hazards and Difficulties of IP Valuation.

Difficulty in Recognizing the Actual Ownership.

Identifying the legal ownership of intellectual property is considered one of the initial challenges of M&A. Important assets such as source code or design rights are not in most instances fully registered, or they can be developed with third parties. In the absence of a proper ownership documentation, it is not certain as to who owns what.

Appreciating Early-stage/Emerging technologies.

Startups and innovation-oriented companies usually have a good but untested innovation. In these situations, it is very speculative to predict which earnings or which market will be accepted. To come up with believable values, investors and acquirers have to use scenario analysis, sensitivity test, and probability weighted results.

The Issue of Extraterritorial Rights.

IP protection is different in international dealings. A patent that is valid in one nation might not be valid in a different country and brand names may have a trademark conflict. Cross-border M&A thus involves close mapping of the legal defenses in order to prevent over-valuations.

Financial Reporting and Compliance issues.

Purchase Price Allocation and Recognition Rules.

Once a merger or an acquisition has been finalized, according to accounting standards, the buyer has to charge the purchase price to all identifiable assets, including IP. These intangible assets under IFRS 3 should be recognized as intangible assets not linked with goodwill provided that they are measurable and legally identifiable.

This is where professional IP valuation techniques used for M&A and financial reporting under IFRS standards come into play. The use of established valuation procedures by independent experts is done to bring the reported numbers to reflect on the international accounting principles.

Impairment reviews and useful life reviews.

After making a recording, intangible assets should be tested on a regular basis regarding impairment testing in IAS 36 to ascertain that they are not not carried following recoverable value. Trademarks that have indefinite life are tested on an annual basis and those with finite life are amortized. Those practices protect shareholders and ensure the quality of reported financial positions.

Disclosure Obligations and Transparency.

The regulators have placed much emphasis on transparency of valuation assumptions, where level three inputs, which are those that are based on unobservable market information, are to be applied. The companies should also reveal the procedures, major assumptions and sensitivities that may materially impact the fair value. Such revelations increase the level of trust and comparability among market players.

The IP Valuation Experts Role in M&A.

Supportive Audit and independent Assessment.

The nature of IP valuation is too complicated, which is why acquiring companies are commonly based on the help of expert valuation advisors. Not only do these professionals supply numerical estimates but they also assist in audit reviews and regulatory filings. Their autonomy contributes to credibility in the financial statements and reduce the conflict between the buyers and sellers.

Finance Strategy- Bridge.

An effective valuer is one who knows financial modelling and business strategy. They are able to determine what IP assets yield the most value and hence inform their post-acquisition licensing decisions, integration or divestment. Such understanding brings an IP valuation out of compliance to strategic management tool.

Case Insight: Consumer-Sector Acquisition using Brand-Driven.

Take the case of a multinational drinks company purchasing a fast expanding local firm. Even though the target does not have much physical infrastructure, it possesses strong brand names, proprietary recipes, and strong distribution rights.

In the process of valuation, analysts conclude that more than 70 per cent of the purchase value can be related to IP-related assets. The Relief-from-Royalty approach is used to value the brand portfolio, and the proprietary formula is used to value a cost-to-recreate model. The analysis shows that it is customer loyalty and not production capacity that makes the company market value.

Consequently, the acquiring company has strategic integration of these IP assets in its global operations, which has a market appeal and enhances brand consistency in its systems in different locations.

Conclusion

The global deal-making has come to a point of intellectual property. Since M&A deals are more and more risky in the context of innovation and digital resources, the capacity to quantify and protect IP value correctly is the key to positive results.

A strong valuation procedure, which is based on the intellectual property valuation practices as required by the IFRS which is merger and acquisitions and supported by professional IP valuation techniques used in M and A and financial reporting under the IFRS requirement, makes sure that there is transparency which provides more strength in negotiations and investor confidence. In the end, learning how to value IP will enable companies to turn the real strategic potential of any transaction and will catapult sustainable value creation long after the date the deal is closed.