Certified AI and Digital Assets Valuation

Emerging Trends: AI, Digital Assets, and Non-Traditional IP Valuation

Introduction to Certified AI and Digital Assets Valuation

In the era of digital transformation, intellectual property (IP) has evolved far beyond traditional categories such as patents, trademarks, and copyrights. As artificial intelligence (AI), blockchain, and data-centric business models redefine how value is created and captured, new forms of IP—such as algorithms, data sets, digital platforms, and non-fungible tokens (NFTs)—are challenging conventional valuation frameworks. These assets, collectively known as non-traditional IP, have become the cornerstone of competitive advantage in technology, finance, and creative industries.

Traditional IP valuation models were designed for tangible inventions and predictable revenue streams. However, modern businesses increasingly rely on intangible digital assets whose value is driven by user interaction, network effects, and the adaptability of technology itself. As a result, the methodologies for assessing worth, ownership, and risk have become far more complex.

This article explores the emerging trends shaping IP valuation in the age of AI and digital asset valuation under IFRS and IAS 38 and digital assets, examining how innovation, regulation, and financial modeling converge to redefine the meaning of “value” in the modern economy.

The Shift Toward Non-Traditional IP

Redefining Intellectual Property in the Digital Age

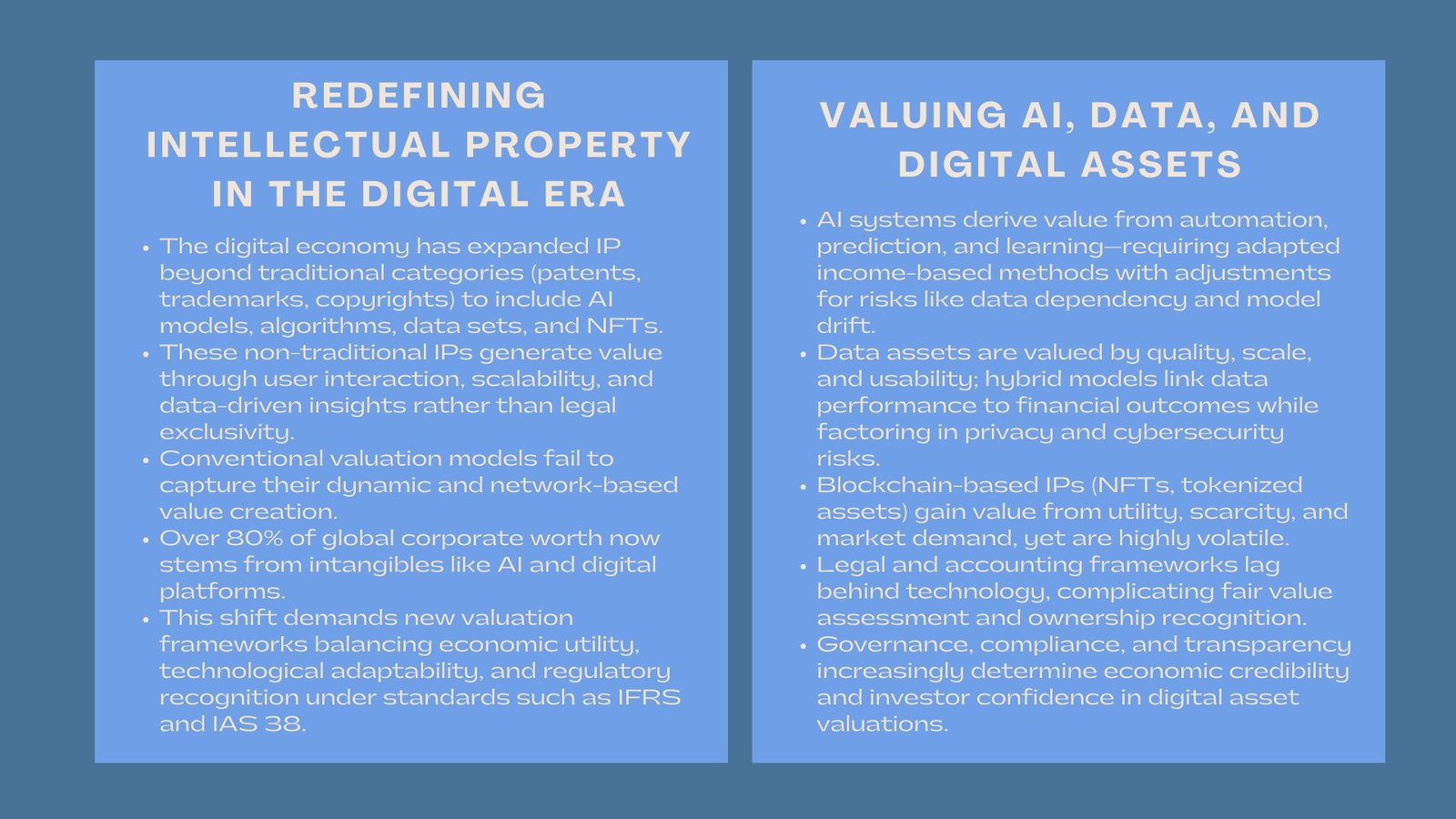

In the past, intellectual property referred mainly to legally protected creations of the mind—patents for inventions, trademarks for brands, and copyrights for artistic works. Today, the scope of IP has expanded to encompass intangible digital constructs that often lack formal legal classification but carry substantial economic value.

For instance, AI models and algorithms are valuable because they encapsulate proprietary logic, training data, and predictive capabilities. Databases and digital user platforms derive value from network participation and behavioral data. NFTs and tokenized assets represent verifiable ownership in digital ecosystems, creating new opportunities for monetization.

These evolving forms of IP do not always fit neatly into existing legal or accounting definitions. Their valuation therefore requires a broader perspective—one that recognizes economic utility, technological uniqueness, and scalability potential rather than relying solely on legal enforceability.

The Rise of Intangible Dominance

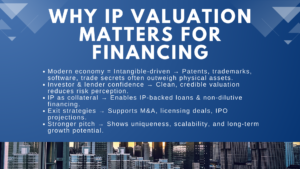

Globally, intangible assets now represent over 80% of total corporate value in leading industries such as technology, media, and pharmaceuticals. A significant portion of this value lies in assets that do not appear explicitly on balance sheets, such as AI algorithms, proprietary datasets, and digital infrastructure.

This shift toward intangibles has transformed how investors and regulators view enterprise worth. Companies like Google, OpenAI, and Meta derive much of their valuation from predictive algorithms and user data networks—assets that traditional cost or income methods cannot fully capture. Consequently, the valuation profession faces mounting pressure to evolve its techniques to ensure relevance, reliability, and compliance.

AI as an Asset: Valuing Algorithms and Machine Learning Models

The Economic Substance of AI

Artificial intelligence systems represent one of the most complex and valuable forms of modern IP. The economic value of AI lies in its ability to automate decisions, predict outcomes, and enhance operational efficiency. Unlike patents or copyrights, AI models are dynamic—they continuously learn and improve through exposure to new data. This adaptive nature makes them both powerful and difficult to value.

AI assets may generate direct revenue through licensing or indirect benefits such as cost reductions and productivity gains. The challenge lies in quantifying these benefits over time, especially when AI performance depends on changing data quality, computational resources, and evolving algorithms.

Methodological Adaptations for AI Valuation

Traditional valuation methods such as the Relief-from-Royalty or Excess Earnings Method must be adapted when applied to AI. The starting point is often an income-based approach that estimates future cash flows attributable to the AI’s deployment. However, additional adjustments are required to reflect unique AI-specific risks such as data dependency, technological obsolescence, and model drift.

Valuation practitioners increasingly combine financial modeling with technical audits—assessing not only the commercial outputs but also the underlying architecture, scalability, and algorithmic robustness. In some cases, hybrid approaches incorporating data science and econometric modeling are used to estimate the relationship between AI-driven predictions and financial outcomes.

Regulatory and Ethical Considerations

As jurisdictions worldwide begin regulating AI—such as the European Union’s AI Act—valuation models must also account for compliance costs, ethical risks, and governance obligations. Non-compliant algorithms may face restrictions or fines, directly reducing asset value. Conversely, transparent and well-documented AI systems tend to command premium valuations due to reduced regulatory risk.

In this sense, the future of AI valuation lies not only in financial forecasting but in responsible innovation and adherence to governance standards.

Digital Assets and Blockchain-Based IP

The Tokenization of Value

Blockchain technology has enabled a new paradigm in asset ownership and monetization. Through tokenization, digital and real-world assets can be represented as cryptographic tokens on decentralized ledgers. Among these, non-fungible tokens (NFTs) have gained attention as a mechanism for establishing authenticity and ownership of unique digital creations—ranging from digital art and gaming assets to intellectual property licenses and digital twins of physical goods.

The valuation of NFTs and tokenized IP requires an understanding of both financial and behavioral economics. Their value is often determined not only by underlying utility or income potential but also by market perception, scarcity, and liquidity. These attributes introduce volatility and speculation, challenging the traditional notion of fair value.

Valuing Blockchain-Based Intangibles

To value blockchain-related IP, analysts typically consider three dimensions: utility, scarcity, and market demand. Utility reflects the functional use of the asset—such as its role in smart contracts or decentralized applications. Scarcity, enforced through blockchain protocols, creates exclusivity and perceived value. Market demand, influenced by user adoption and community engagement, determines liquidity and price stability.

While income-based valuation remains applicable for tokenized assets generating royalty or transactional revenue, market-based approaches—anchored in active trading data—often dominate in practice. However, these valuations are inherently sensitive to speculative cycles, making consistent measurement a significant challenge for financial reporting.

Legal Recognition and Accounting Challenges

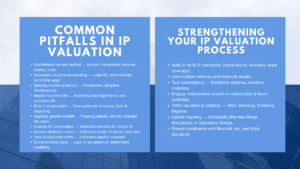

The legal and accounting treatment of digital assets remains fragmented globally. Some jurisdictions recognize tokenized IP as intangible assets subject to revaluation under IFRS or local GAAP, while others classify them as inventory or financial instruments. This lack of standardization complicates the task of valuation and financial disclosure.

Moreover, questions of ownership and jurisdiction—particularly in decentralized systems—further blur valuation boundaries. As legal frameworks evolve, the ability to clearly define rights, obligations, and transferability will determine how digital assets are recognized and measured in mainstream financial systems.

Data as a Strategic Intangible Asset

From Resource to Revenue Generator

Data has emerged as the most pervasive non-traditional intangible asset in the digital economy. Companies derive immense value from collecting, processing, and analyzing data to improve decision-making, personalize services, and create competitive differentiation. In many cases, proprietary datasets form the foundation of AI algorithms, customer analytics, and market intelligence platforms.

The valuation of data as an asset involves understanding its quality, uniqueness, relevance, and potential for monetization. Unlike patents or copyrights, data value is not derived from exclusivity but from scale, accuracy, and usability. Thus, its worth depends on how effectively it can be transformed into actionable insights or commercial products.

Valuation Challenges for Data Assets

Traditional valuation approaches struggle to capture the multifaceted nature of data. The cost-based method often underestimates value since data creation and storage costs do not reflect its analytical potential. Income-based methods face difficulty in attributing incremental revenue directly to data usage.

To address these challenges, hybrid approaches have emerged, combining statistical modeling, econometric analysis, and scenario simulations. These methods attempt to link data-driven activities with measurable financial outcomes—such as increased sales conversion or operational efficiency. Additionally, data valuation increasingly incorporates risk factors such as privacy compliance (GDPR, CCPA), cybersecurity, and data obsolescence.

The Role of Governance in Data Valuation

Data governance—the framework that regulates collection, usage, and security—has become a key determinant of value. Companies with robust governance structures and transparent consent mechanisms tend to command higher valuations for their datasets. Conversely, entities that fail to meet regulatory standards face impairment risks, fines, and reputational damage.

Hence, the valuation of data assets is no longer purely a technical exercise but a holistic process integrating finance, compliance, and ethics.

Integrating Technology and Financial Modeling

AI-Driven Valuation Models

Ironically, AI itself is transforming the field of valuation. Machine learning algorithms are increasingly used to forecast intangible asset performance, identify market comparables, and analyze large data sets. Predictive analytics enables real-time revaluation of assets based on market sentiment, user engagement metrics, and transactional behavior.

AI-driven valuation tools enhance consistency and reduce bias by processing vast information beyond human capability. However, they also introduce new questions about transparency and explainability. Regulators and auditors now emphasize the need for human oversight in algorithmic valuation to ensure accountability and interpretability of results.

Blockchain and Smart Contracts in IP Management

Blockchain is also revolutionizing how IP rights are recorded, licensed, and monetized. Smart contracts allow automatic enforcement of licensing terms, royalty distribution, and usage tracking, creating immutable audit trails. This transparency enhances the defensibility of valuation assumptions by providing verifiable transaction data.

In future, blockchain-based registries could become standard for IP ownership verification, reducing legal uncertainty and valuation risk. The integration of blockchain into IP management may thus foster a more efficient, transparent, and liquid market for intangible assets.

Implications for Tax, Accounting, and Regulation

The Need for Updated Standards

The rapid evolution of non-traditional IP exposes a growing gap between technological reality and regulatory frameworks. Existing accounting standards such as IAS 38 and IFRS 13 were designed for static intangible assets with clear ownership rights. They do not adequately address algorithmic adaptability, decentralized ownership, or data monetization.

Tax authorities face similar challenges. Determining the fair value of digital assets for transfer pricing or tax purposes is complicated by fluctuating markets and uncertain economic substance. As a result, regulators and standard-setters are exploring revised frameworks to better capture the unique characteristics of digital and AI-based assets.

The Role of Independent Valuation and Assurance

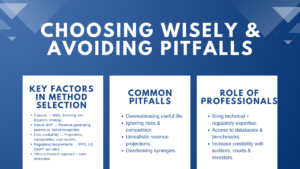

Given the complexity of emerging IP, independent valuation and assurance have become critical. External experts not only provide technical rigor but also enhance transparency and credibility for investors, auditors, and tax authorities. Independent reviews ensure that methodologies remain consistent, assumptions reasonable, and conclusions defensible within evolving regulatory landscapes.

Benefits of Recognizing and Valuing Non-Traditional IP

Strategic Insight and Competitive Advantage

Recognizing and valuing non-traditional IP allows companies to understand the true sources of their competitive advantage. By quantifying the contribution of algorithms, data, and digital platforms, management can allocate resources more efficiently and prioritize innovation that drives enterprise value.

Investor Confidence and Market Transparency

Transparent valuation of digital assets enhances investor confidence by revealing hidden drivers of performance. It allows markets to better differentiate between firms based on the sustainability of their intangible value rather than speculative market sentiment.

Compliance and Risk Management

A structured approach to non-traditional IP valuation supports compliance with emerging global standards while mitigating reputational and regulatory risks. It ensures that intangible assets are managed, disclosed, and taxed appropriately, reflecting both economic reality and ethical responsibility.

Conclusion

The world of intellectual property is undergoing a profound transformation driven by artificial intelligence, data, and digitalization. Traditional valuation methods—built for static, legally defined assets—are being reshaped to accommodate dynamic, interconnected, and often decentralized forms of value creation.

As AI models, digital assets, and data ecosystems continue to redefine business models, non-traditional IP valuation will become central to financial reporting, how to value non-traditional intellectual property assets, strategic management, and regulatory compliance. The challenge for valuation professionals lies in blending financial acumen with technological literacy, ensuring that modern assets are measured not just by cost or law, but by their capacity to generate sustainable innovation and economic impact.

Ultimately, the future of IP valuation will depend on a new equilibrium—one where finance, technology, and ethics converge to define the next generation of intangible value in a world where intelligence itself has become the most valuable asset.