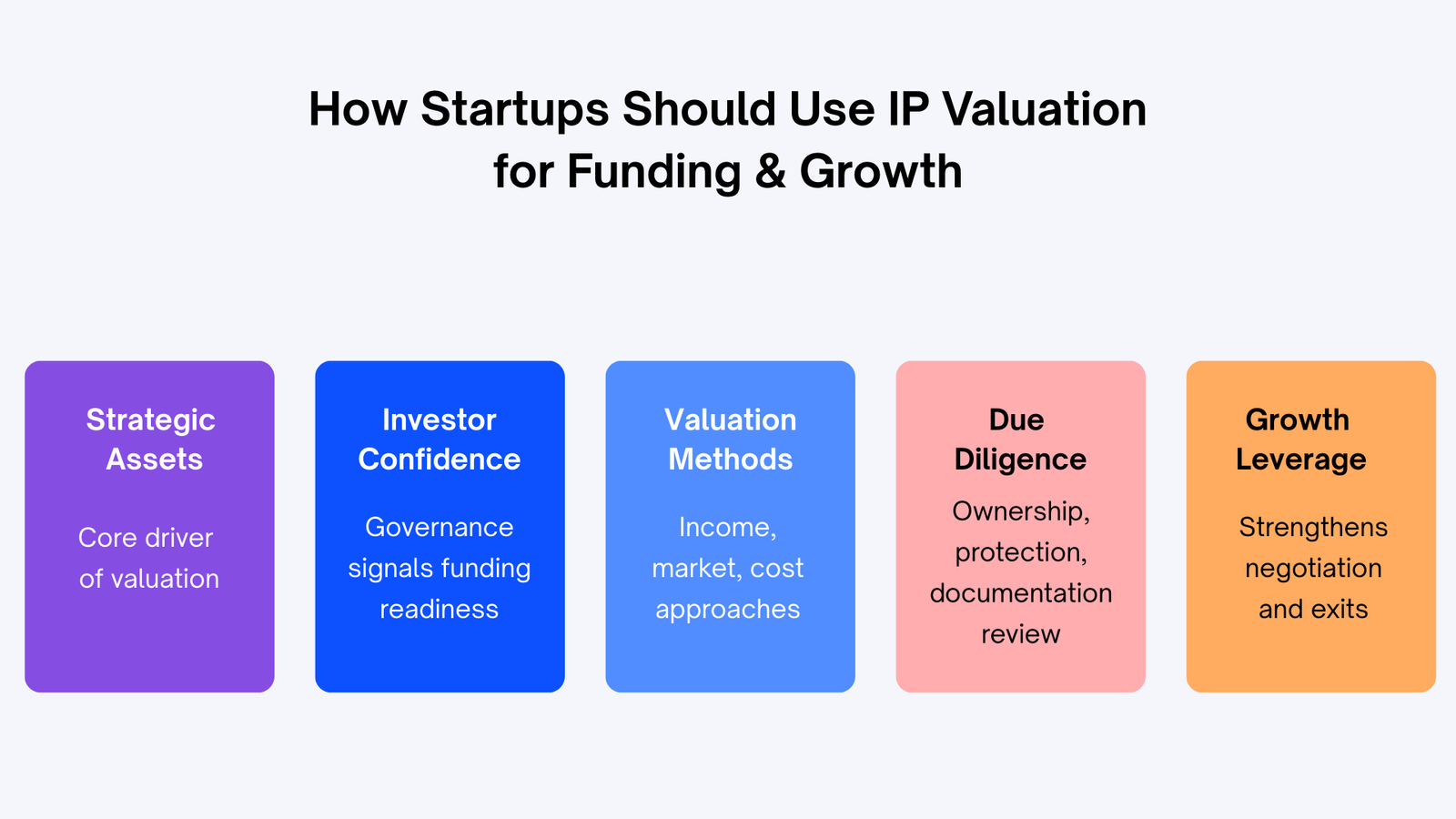

How Startups Should Use IP Valuation

for Funding & Growth

Introduction to How Startups Should Use IP Valuation

The correlation between IP Valuation and the Success of Startup Funding

The distinction between a convincing pitch and a transformative pitch in the hyper-competitive environment of startup-fundraising is frequently reduced to a single, poorly used asset intellectual property. The presence of founders who know and can explain the value of their IP is not only more likely to set them in a better position to negotiate with investors, but it makes them inherently better-placed to be able to command higher pre-money valuations, negotiate with favourable term sheets, and raise the type of capital their ambitions demand.

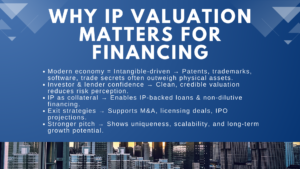

IP valuation of startups entails the systematic method of estimating the economic value of the intellectual property of a company: its patents, trademarks, trade secrets, computer software programs, proprietary algorithms, and data assets held by customers. In a world where intangible assets constitute overwhelmingly significant share of enterprise value in the technology, healthcare, fintech and digital services industries, the IP value measurement and communication capability has become a competitive advantage of founders, CFOs and boards.

The startup ecosystem in Singapore has evolved to a great extent in the last ten years. As the amount of venture capital being invested in the region has over S$15 billion annually in Southeast Asia, and Singapore has become the regional headquarters to a significant portion of that capital which is increasing every year, the level of investor preparedness has risen accordingly. Structured IP due diligence Singapore has become a regular aspect of deal analysis by investors at all levels, including seed rounds, pre-IPO, and others. The startups that enter this process unprepared are subjected to unnecessary valuation discounts and delays in deal.

What Matters to Investors about Intangible Value

Durability is the core issue of concern to investors as far as IP is concerned. Start up competitive advantage can be based on a varied number of sources such as a strong talent pool, first mover, or a good time in a market, but only IP generates a legal barrier to competitors that can not be replicated. A proprietary set of data that is contractually secured by a patent, a well-registered collection of trademarks, or even just a proprietary technology that is defended by a patent offers a degree of defensibility that is not achievable by the speed of execution.

The IP assets also offer downside protection as viewed by an investor. In distressed sale or wind-down situation, IP assets, having proven fair value can be sold, licensed, or assigned – to ensure a recoverable floor on investment value. A startup with S$3 million in independently-valued assets of patents has a materially different risk profile as compared to that of a startup whose entire valuation is based on an untested product concept.

The individual deal is not the only beneficiary of the intellectual property valuation. When a startup invests in IP valuation, it shows the market that its founders are careful in their thinking regarding value creation, governance, and defensibility over the long term, which are the attributes that help fundable companies pass through the Series A round.

What is IP Valuation?

Definition and Scope

Startup IP valuation is the organised approach to the estimation of the economic worth of certain intellectual property holdings – individually or in a bundle – by recognised valuation procedures that may be undertaken by competent professionals. An IP valuation yields a fair estimation of supportable, documented fair value that is capable of being utilized to negotiate fundraising, financial reporting, as well as licensing deal structures, mergers and acquisitions or dispute resolution.

The level of IP valuation relies on the intention. A pre-funding IP valuation may concentrate upon two or three of the most commercially relevant property of the startup the core technology patent, the brand trademark, and so on. An integrated acquisition related IP valuation according to the IFRS 3 Purchase Price Allocation requirements will be applied to value all identifiable intangible assets on basis of all categories. The cost of a licensing negotiation may involve a one-asset relief-for-royalty study to determine an arm-length royalty rate.

Intellectual property that is typically considered startup worthy is: granted and pending patent; registered trademarks and brand equity; proprietary software and platform code; customer databases and relationship assets; trade secrets and algorithm secrets; licensing agreements and franchise licenses, and regulatory approvals or government licences of transferable value.

These are the differences with General Business Valuation

The IP valuation has a few fundamental differences with the general business or enterprise valuation. Business valuation is an estimation of the total equity or enterprise value of a business, the amount that a buyer will pay to acquire the entire business. IP valuation, in contrast, values individual assets of that business because different assets produce different cash flows, have varying risk profiles and useful lives.

One of the main differences made in IP valuation of startups is the necessity to separate the economic contribution of each IP asset to the business as a whole. Some startup may be able to make S$5 million in revenue, but the IP valuation process needs to compute how many of that income can be attributed to the technology patent and brand and customer relationships (and what each of those income streams would be worth individually). The technical aspect of disaggregation is challenging but is a requirement in order to ensure that the benefits of credible intellectual property valuation are realised in the context of negotiations and due diligence.

When Startups Need to do IP Valuation

Pre-Seed and Seed Stages

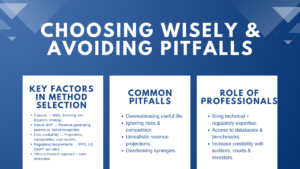

The pre-seed and seed is the first level where the IP valuation of startups will provide tangible value, especially when the startup is submitting government grants, a request to a finance source based on IP, or about to enter an angel investment. It might be too early to be able to perform a complete income-based IP valuation at this point — the startup does not have the revenue history and market validation to justify projected cash flows. Nevertheless, a cost assessment of development investment can offer a helpful baseline, along with a preliminary IP landscape analysis.

At the pre-seed stage, the more actionable interventions include IP audit and strategy development: listing all IP the company has developed or will develop, what should be registered IP (patents, trademarks, designs), the IP ownership of the company should be cleanly vested in the company entity (not in individual founders), and documentation practices are required that will facilitate the valuations in the future. These are base case steps that are of insignificant cost but provide grossly disproportionate value upon entry into the initial institutional fundraising preparations of the startup.

Before VC or PE Rounds

The most commercially significant time in which a formal IP valuation can be applied to startups is in the months preceding a large VC or PE round of financing. By this stage, the startup is usually commercial enough with revenue, customer base, growth curve, etc., to justify an IP valuation based on income. A pre-independent valuation report created prior to the start of the investment process achieves several purposes: it educates the founders about their own perception of the value of their IP, it gives a justifiable point of departure in pre-money valuation negotiations, and it pre-empts the IP-related aspects of IP due diligence Singapore that the investor will undertake.

Timing matters. The process of conducting an IP valuation report that is prepared 6 months prior to a fundraise allows the founders to fix any deficiencies in the IP valuation report, such as submitting missing trademark applications, finalising trade secret paperwork, or clarifying the ambiguity of IP ownership, before the legal counsel of the investor identifies those deficiencies. IP valuation prepared under time pressure during the due diligence process of the investor is less likely to be comprehensive and more likely to create queries that would postpone close-out of the deal.

Pre-M&A or Acquisition Talks

Independent IP valuation of startups is necessary when it comes to a possible sale of a trade, merger, or strategic partnership. The acquirer will do their own IP due diligence and attribution exercise – normally as part of a comprehensive Purchase Price Allocation under IFRS 3 – and will develop a personal opinion of IP value. A startup which has already undergone independent IP valuation is much better off to converse, and potentially dispute, with the attribution deductions of the acquirer.

The attribution of purchase price of IP assets, goodwill, and other elements in M&A negotiations have a direct impact on the economics of the deal such as what will be the tax treatment of the deal in Singapore and in any other cross border jurisdictions. A credible, documented IP valuation by a startup can better negotiate on the allocation of consideration to particular assets to optimise the headline price as well as after-tax result.

IP valuation at exit has significant implications on the startup growth strategy. It is always founders who recognize the importance of their IP portfolio, who develop the portfolio strategically and defensively, who will succeed whenever they attempt to go through the trade sale process than those who consider IP as an afterthought.

Start up benefits of IP Valuation

Competitiveness in Negotiation

The most urgent intellectual property valuation advantages to the startups in a fundraising or a M&A scenario is the bargaining power. By a founder being able to demonstrate an independently validated IP valuation – backed by recognised methodology, market data and professional credit – he turns the discussion on pre-money valuation into a negotiation of evidence rather than a negotiation of opinion. Investors and acquirers would treat valuation arguments based on documented analysis with more respect, will interact with them and ultimately accept them.

This is especially useful in the context of deep technology startups where the main assets are patents and proprietary software that is not easily assessed by investors unless with the input of a specialist. A relief-from-royalty valuation which proves that a technology patent is worth S$4 million through what can be observed based on licensing market data is much more convincing than what a founder can assert that the patent is valuable. The detail and approach of the valuation forms a platform of constructive negotiation and not a stalemate over the baseless standing.

Higher Investor Confidence

Out of the negotiating table, IP valuation of startups is an indicator of governance maturity to investors. The fact that a startup has made an effort to fund independent IP valuation (as opposed to management estimates) indicates that the management of the company takes financial rigour seriously, recognizes the significance of intangible asset management, and has established the professional relationships (with valuers, IP lawyers, and financial advisers) required to facilitate complex growth strategies.

This control indicator especially matters to institutional investors which include family offices, VC funds and PE firms that are putting in place the money of other people and therefore have fiduciary duty to carry out a due diligence. When an LP of a VC fund queries a VC fund as to why it invested in a specific company the LP would want to know that the team did due diligence IP Singapore and that the IP value has been independently verified not that the fund relied on the word of the founder.

Enhanced Deal Transparency

IP valuation also enables the deal transparency which is a precondition to a successful deal. In the case where both the parties in a fundraising or M and A process are privy to the same IP evidence of valuation, negotiations can be based on strategic fit, growth potential and deal structure, as opposed to being mired down in underlying contentious issue regarding the actual value of the company. Transparency helps to speed up the deal timelines, minimize the legal expenses, and generate trust between the founders and investors needed in long-term collaboration.

The transparency of intellectual property valuation is also beneficial even after the transaction. Those investors with an established, documented knowledge of the IP they have invested in are more likely to be the partners in the post-investment process – they can have a role to play in IP commercialisation strategy, licensing negotiations, and exit planning, as opposed to finding out the IP landscape when a crisis strikes.

Practices with IP Valuation Methods

Valuation based on income: DCF and Relief-from-Royalty

The most theoretically sound methods of IP valuation of startups are income-based, and these are the most common in licensing deals, M&A due diligence, and financial reporting. There are two major income-based approaches, namely:

Discounted Cash Flow (DCF) / Excess Earnings: According to the excess earnings approach based on DCF, the value of an IP asset is derived by forecasting the cash flows after tax and attributable directly to the asset and discounting them to the present value at a risk-adjusted discount rate. In the case of startup technology assets, this would entail revenue estimates, a margin analysis and determination of the useful economic life of the IP. Multi-Period Excess Earnings Method (MEEM) is a continuation of this framework, but with an explicit modelling of contributory asset charges – such that the IP value only incorporates the incremental cash flows arising beyond the contribution made by other business assets.

Relief-from-Royalty: In this technique, IP value is computed by capitalising on the royalty payments that the startup would make had the asset not been owned, but licensed. It is usually used in brands, patents and technology assets. The approach needs a justifiable royalty fee – based on similar database licensing deals in databases like RoyaltyRange or ktMINE – and revenue estimates throughout the remaining useful life of the IP. The relief-from-royalty technique is especially suitable to the situation of IP due diligence Singapore since it grounds the value on the observable market rhythms and, as such, is quite defensible to both investors and the audit team.

Comparisons of Technological Startups in the Market

The market strategy attributes value to IP based on prices paid in similar IP assets to recent transactions, either in patent sales, brand acquisitions, software licensing deals or franchise acquisitions. In the case of tech startups, any market data also pertinent to the valuation of the target would involve the price of reported patent transactions on the Patent Exchange or reputed M&A transactions, and SaaS business valuation data.

Market approach is mainly a corroborative approach and not one of the main approaches in IP due diligence Singapore practice since it is often hard to find transactions that are truly comparable when handling new start-up IP. Nonetheless, market comparables are necessary to prove the reasonableness of incomes based conclusions, in the case that a relief-from-royalty valuation concludes on a brand value of S$8 million of a startup with S$3 million in annual revenue, the market comparable transaction records can either justify or oppose that finding in brand acquisitions within the same industry.

Cost and Replacement Cost Methodologies

The cost method calculates IP value upon the amount of money that is needed to reproduce or substitute the asset. In IP valuation of startups there are two variants used:

Historical cost method: Sums up all recorded R&D, development, legal and registration expenses that were incurred in developing the IP asset. Easy to implement based on the financial records of the startup, though can be overly low when breakthrough innovations are involved with the market value much higher than the development cost.

Replacement cost method: Approximates the present-day price of re-creating a similar asset as a new asset i.e. the developer-hours and cloud infrastructure cost of re-creating a proprietary software platform at the current market rate. This is more indicative of the current market value compared to the historic cost and it is especially applicable to the software and database assets.

The cost method is best used at the pre-revenue stage where the income estimates are too speculative to estimate a viable DCF, and market comparables are few. It offers a justifiable lower limit on IP value and is applicable to grant programs, IP-supported loan programs, and pre-investor conferences. Its main shortcoming is that it fails to reflect the value of the prospective earnings of the market – which in a breakthrough technology can far surpass the development cost.

The IP Valuation and Due Diligence

What Investors Look For

When institutional investors are carrying out IP due diligence Singapore, they are performing a number of different dimensions of quality of IP at the same time. Knowing what investors seek and can do, is one of the most profitable activities that a company can engage in before a fundraise.

| Due Diligence Dimension | What Investors Assess | Common Red Flags |

| Ownership & Title | Is IP cleanly owned by the company entity? Are all founder, employee, and contractor IP assignment agreements in place? | IP registered in founder’s personal name; no assignment agreements with contractors |

| Registration Status | Are patents pending or granted? Are trademarks registered in key markets? Are domain names and social handles secured? | Key marks unregistered; patents lapsed; no international trademark strategy |

| Freedom to Operate | Does the startup’s product potentially infringe third-party IP? Has a freedom-to-operate analysis been conducted? | No FTO analysis; unresolved cease-and-desist notices; use of open-source with restrictive licences |

| IP Valuation | Has an independent valuation been conducted? Are the methodology and assumptions credible and well-documented? | No valuation; valuation prepared only by management; unsupported royalty rate assumptions |

| Commercialisation | Is the IP generating revenue, licensed, or on a credible path to commercialisation? | Patent filed but product never launched; brand registered in wrong classes |

Preparation of IP Documentation

Proper planning of IP due diligence Singapore involves the arrangement of IP documentation to a clear and accessible data room which would allow the investor counsel to properly review all the materials. An organised IP data room must contain:

IP register: A detailed list of all IP property, including patents, trademarks, copyrights, domain names, trade secrets, all including registration numbers, filing date, jurisdiction, ownership, and the renewal status.

IP assignment agreements: Signed agreements between all founders, employees, and contractors where the company is assigned IP created on its behalf.

IP valuation report: An independent professionally prepared valuation report of the material IP assets of the startup, prepared on recognised methodologies, and with well documented assumptions.

Freedom-to-operate analysis: A legal decision affirmed that the products of the start up do not violate third-party patent and other intellectual property rights.

Licensing agreements: All inbound and outbound licences, open-source licence compliance documentation and third party technology licences.

IP policy records: record of employment IP policy, templates of NDA, and confidentiality procedures which show that trade secrets are actively secured.

Typical Areas of Vulniching in Startup Due Diligence

Although IP is important in the value of startups, some of these gaps are glaringly common in the process of IP due diligence in Singapore. These are some of the most frequent areas of failures that founders can anticipate and deal with beforehand:

IP ownership not property of the company: This is common with startups based on the academic work or past worker developing IP in his or her own capacity before the company was established. The concept of retroactive assignment can be complicated and expensive.

None registered in Singapore or target markets: Founders pay too much attention to product development and not to brand protection to realize too late that another competitor has registered his/her brand name or logo.

Contamination of open-source licences: Incorporation of open-source software components with viral licences (including GPL) in proprietary products may create encumbrances in IP that investors may consider material risks in the case of viral licences which mandate that requirements of a derivative work be also open-sourced.

No invention documentation: In patent cases, date of invention can prove important in cases of priority issues. Startups that do not have lab notebooks, version control logs, or other records of invention documentation are weak in contested proceedings.

Dependence on management prepared IP valuations: Investors and their advisers will discount or ignore self-prepared valuations which are not based on independent, methodologically rigorous, or market-based preparations.

IP Strategy and Company Valuation

The IP Value Effect on the overall Enterprise Value

The correlation between IP strength and overall enterprise value is not only thoroughly developed in the business book of corporate finance, but it is also found in the practice of IP due diligence Singapore on a day-to-day basis. The higher the quality of IP portfolio, that is more defensible, the greater the revenue multiple, lower cost of capital, and superior acquisition premiums the startup will command, compared to structurally similar business with weaker IP situations.

The principle is simple in nature, IP assets increase the lifespan and stability of competitive advantage of a startup. A company that is capable of defending its market position over a decade by patents and trademarks generates more predictable cash flows – and thus deserves higher valuation multiple – than one whose benefit mere deep-pocket rivalry can duplicate in 18 months. This exact duration premium is explicitly represented in the discounted cash flow models in terms of longer projection horizons, lower terminal year attrition assumptions and lower risk premiums.

In the case of a startup growth strategy where defensible market position development is a primary goal, IP investment is thus not a cost, rather a driver of valuation. Each dollar invested in patent application, trademark registration and IP clearances earns the enterprise value of a multiple of the amount invested in it, in the form of a competitive moat.

Tech and Digital Startup Examples

The advantages of the intellectual property valuation can be demonstrated by a number of typical situations prevalent in the technology and digital start-up scene in Singapore:

| Startup Type | Primary IP Assets | IP’s Role in Valuation | Estimated IP as % of EV |

| SaaS / B2B Platform | Proprietary software, customer data, brand | Technology and customer relationship value drives ARR multiple premium | 50–65% |

| Deep Tech / Biotech | Patents (core innovations), trade secrets | Patent pipeline is the primary value driver; enterprise value is essentially an IP bet | 70–90% |

| Consumer Brand / D2C | Trademark portfolio, customer database, brand equity | Brand premium supports pricing power and customer lifetime value assumptions | 40–60% |

| Fintech / Regtech | Algorithms (patents or trade secrets), regulatory licences, brand | Regulatory licences and proprietary models create high barriers to competition | 55–75% |

| Marketplace / Platform | Brand, network effect data, technology, contracts | Brand and network data are the primary defensibility assets in a winner-take-most market | 45–65% |

These scopes help to explain why IP valuation of startups is not a side-story to the enterprise valuation discussion – in most of the technology and digital companies IP is the enterprise. Any startup growth strategy that does not take into account IP building and protection is, in very real sense, a strategy that does not take into account value creation.

Startup Growth IP Governance

Board Oversight and IP Policy

With the rise in size of a startup, IP governance (systems and methods under which the company identifies, protects, manages, and monetises its IP) is a factor of increased significance in overall corporate governance. IP oversight should also be on the boards of directors agenda of growth stage start-ups, with boards making sure that the IP portfolio is congruent with the start-up growth strategy and that emerging IP risks are prioritized and proactively dealt with.

The documents every growth-stage startup ought to have in place to define the scope of IP governance include: an IP policy which explains what the company considers its IP, how it will be documented and reported; an NDA and confidentiality policy which normalises the approach to protecting trade secrets in all its external interactions; and an IP register which is maintained and updated on a regular basis as more IP is created or acquired.

In the case of startups that have been institutional investment, post-investment IP reporting is another aspect that is expected of the IP due diligence Singapore by the investors. Growth-stage companies are required by their investors to submit periodic updates on IP progress in a regular IP update letter such as the status of patent applications, trademark renewals, and infringements as part of their constant portfolio assessment.

Measuring IP Performance Metrics

It is necessary to have the data to measure the performance of the IP portfolio of a startup that goes beyond the number of patents or trademarks applied. The meaningful IP performance metrics to be used in a startup growth strategy will include:

IP coverage ratio: The ratio of core product features or business lines covered by granted or pending IP protection, -a measure of the extent to which the competitive advantages of the business are legally defended.

IP value as a percentage of enterprise value: This ratio is over time, and it shows that the startup is generating IP value relative to its overall growth.

Royalty and licensing Revenue: In the case where the startup has actively licensed IP, the commercial productivity of the portfolio is determined by the revenue collected as royalty per IP asset.

Time-to-filing: The mean duration between the time after developing an invention or brand and the time when the corresponding IP application is actually filed – a parameter of IP identification process efficiency.

IP maintenance cost as a percentage of revenue: Makes sure that the IP protection expenses are kept in check as the business grows, and stops unnecessary IP of the portfolio.

Case Studies and Work Examples

Hypothetical 1 Hypothetical example of SaaS Startup Pre-Series A

Take an example of a Singapore-based B2B SaaS start-up company – “DataStream Pte. Ltd.,” which is building its own data analytics solution to logistics firms. Prior to their Series A round: DataStream has a core data normalisation algorithm pending patent, a 120 percent net revenue retention rate and annual recurring revenue (ARR) of S 1.8 million without IP valuation. Investors are at a SG12 million with the excuse of execution risk and pending (yet to be granted) patent. Negotiation stalls. With independent IP valuation: DataStream has an independent IP valuation commissioned six months prior to the fundraise. The valuation of the pending patent (and a relief-from-royalty method with a 35% pending-grant discount applied using risk-adjusted discounts) and proprietary database are valued at S$4.2 million and S$2.1 million respectively. The investors receive the valuation report prepared by a credentialed independent valuer at the beginning of the due diligence. Investors use the IP valuation as a plausible input, negotiations are centered around the growth assumptions and not the ownership of IP and DataStream is closed at S$16.5 million pre-money which is S$4.5 million above what the investor originally contributed.

Hypothetical Exercise 2: Deep Tech Startup Pre-Acquisition

BioSense Technologies Pte. Ltd. is an Singaporean-based medical device startup having a patented biosensor technology that can be applied in wearable health monitoring. Four years of R&D later, the company has three granted patents, two applications pending and a product that has been CE-marked and early clinical use in Singapore and Malaysia. IP Valuation Result: The independent IP valuation values the patent portfolio (based on a risk-adjusted MEEM across the three key markets) at S$18.5 million, the proprietary manufacturing know-how at S$4.2 million (cost approach, replacement cost basis) and the CE marking and regulatory approvals at S$2.8 million (with-and-without approach, modelling 18-month re-approval period). Total IP fair value: S$25.5 million — compared to the implied IP attribution of S$15 million on first offer by the acquirer. With the independent valuation, BioSense agrees to buy the company at S$38 million or an uplift of S10 million that can be directly linked to the IP valuation exercise.

Common Valuation Outcomes

In IP valuation of startups engagements in Singapore, various trends are repeated:

The art of overvaluing technology patents that are not individually rated: Founders and investors often underestimate the value of the pending portfolio of patents, especially in deep technology subsectors where the sales potential of the underlying technology is many times greater than the current commercial momentum of the startup.

Brand value ignored in B2C startups: Consumer startups which have high brand recognition and customer retention frequently have high values in terms of trademark and brand equity which is never put to the test on paper – value that comes to light at the time of acquisition.

Data on customers as an underestimated IP property: Customer proprietary datasets, such as purchase history databases, usage pattern data, health records are growing into material IP value, and specifically made commercially productive when AI and machine learning applications are utilized. This category of value is not usually included in self-prepared startup IP assessment.

Coingate, costly to remediate at due diligence IP remediation is expensive: Startups that identify IP holes during investor due diligence, such as missing assignments, unregistered marks, open-source contamination, tend to incur S$50,000200,000 legal fees to remediate IP, and can receive valuation discounts or conditioned on such discounts. This is prevented in early IP housekeeping.

Conclusion

Future of IP Valuation in Singapore Startup Ecosystem

The startup ecosystem in Singapore is at the inflection point of the relationship with intellectual property. At the beginning of past decade, IP remained a field of a big multinational and research institute, and was a compliance issue that was left to the periphery of business reality at small start ups. The world has changed today. IP-intensive startups IP-intensive startups in fintech, healthtech, deep technology and digital platforms are the bulk of venture capital activity, and the quality of IP strategy and valuation has become a defining factor in funding results and exit success.

The importance of IP valuation of startups will only rise when Singapore persistently becomes the innovation hub in Asia. The infrastructure, experience, and market norms which will turn IP valuation into a mainstream and not a specialist practice are being actively constructed under government initiatives, such as the IPOS IP Financing Scheme, Enterprise Singapore IP growth programmes, and the Singapore IP Strategy 2030. Qualified IP valuers are becoming more available, there are standardised methodologies and platforms of digital IP data, which are lowering the cost and effort of gaining professional IP valuation support.

To the founders, the message is straightforward, the value of intellectual property as a message is not hypothetical it is real, practical, and can be realized with the correct preparation and expert assistance. It is the startups that formulate deliberate IP portfolios, invest in independent valuation, and align the startup growth strategy with the IP strategy since the earliest stages that raise at the valuation their technology is worth, pass IP due diligence Singapore without painful surprises, and provide the best results to their founders, employees, and investors.

The knowledge economy does not make IP a legal formality. It is the best thing a startup can create – and those startups that comprehend it will be the ones that will shape the decade of innovation that will come to Singapore.