How to Measure Trademark and Brand Value

A trademark or a brand name is not a logo or a tag line to many companies, and it is one of the most important items on the balance sheet. However, the value of that is hardly ever easy to measure. A brand does not carry any price tag as opposed to machinery or real estate. It is only as valuable as it is perceived, as it is as old as it is, or as it is as strong as the law. Learning to quantify trademark and brand value is thus a very important ability to practitioners in the field of finance, marketing, legal and strategy.

This paper describes the fundamental trademark and brand valuation techniques that are applied in practice, follows through the steps and issues involved, and uses the examples of practice to describe what professionals have learned. Having a field guide, you are either coming into the field or trying to refine your knowledge of brand and intellectual property valuation, you will have a strong basis to start with.

With intangible assets taking up more and more corporate valuations, making up over 90 percent of market value of S and P 500 companies as per some estimates, those professionals with knowledge of trademark valuation will become more and more useful to their organisations. Understanding these concepts will put you in an excellent position to make a contribution in the field of licensing negotiations, mergers and acquisitions, litigation support, financial reporting and brand strategy decisions.

Why Trademark and Brand Valuation Matters

A trademark is a legal right a word, symbol, design or any combination, which makes the goods or services of one party to be different than that of another. A brand however is a wider commercial construct that entails the customer experience, reputation and associations accrued to such trademark over the years. When the trademark valuation is conducted by the professionals, they are generally trying to determine the economic contribution which this legal right and commercial identity bring to a business.

A number of real-life situations need brand and intellectual property valuation. They are mergers and acquisitions (a buyer should know what he is paying), license deals (a royalty rate must be negotiated), litigation and claims of damages (a court has to know the economic consequences of infringement), and financial reporting, especially under accounting standards such as IFRS 3 or ASC 805 (which insist on recognizing acquired intangible assets at fair value).

Internal decision-making is also dependent on brand value. Decisions regarding how much to invest in marketing, brand extension strategy, and portfolio management can be made more easily by companies that monitor the financial contribution of their brand through the years. The trademark and brand valuation methods thus fulfill the external reporting as well as internal strategic purpose and hence are unavoidable in current business.

Table 1: Common Scenarios Requiring Brand Valuation

| Business Scenario | Primary Purpose | Typical Stakeholder |

| Mergers & Acquisitions | Due diligence and purchase price allocation. | CFO, M&A, Auditors. |

| Licensing Agreements | Establishing a reasonable royalty charge. | Law, Business Development. |

| Litigation / Infringement | Measuring losses or profit losses. | Attorneys, Judicial Systems. |

| Financial Reporting | Intangible assets recognition by IFRS / GAAP. | Finance, External Auditors. |

| Internal Strategy | Budgetary allocation, brand extensions decisions. | Strategy Teams, Marketing. |

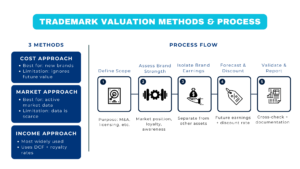

Three Core Trademark and Brand Valuation Methods

Three wide methods are the basis of trademark and brand valuation techniques in the world. These are the market approach, the cost approach and the income approach. They each make sense, and they each have data requirements and the way to use them. The practitioners usually look at all the three and choose the most appropriate technique depending on the purpose of the valuation and data availability.

In the cost approach, brand value is estimated by determining the cost that would be incurred to reproduce or substitute the brand. This could be historical advertising cost, cost of legal registration and time required to create awareness in the market. Although it is easy to implement, it usually undermines the actual worth of an established brand since the method fails to reflect the possible income in the future or the price the customers can afford to pay.

The market approach establishes value by the comparison of the brand to the other brands which have been sold or licensed in an arm-length deal. This is conceptually attractive – it is what the market will actually pay – but it must have similar data which is commonly hard to obtain with unique brands. The most commonly practiced method, the income approach, is a discounted approach to the future economic benefit of the trademark, especially in the valuation of trademarks in M&A and licensing situations.

Process Flow 1:Step-by-Step of Income Approach

| Step | Action | Key Output |

| 1 | Determine the sources of revenue associated with the brand. | Brand-based revenue projection. |

| 2 | Isolate brand contribution by application of a royalty rate or margin. | Earnings/ royalty savings on a brand basis. |

| 3 | Earnings of brand during the rest of the useful life. | Earnings projection over a number of years. |

| 4 | Identify a relevant rate of discount (risk-adjusted). | Weighted cost of capital/ WACC. |

| 5 | Projection of earnings to present value. | Brand value (net present value) |

In the income method, the Relief from Royalty (RfR) method is a common sub-method. The concept is straightforward, in case the firm did not own its trademark, it would license it out to a third party and pay a royalty. The present value of royalty savings avoided hence is the value of owning the trademark. The popularity of the RfR method is due to the fact that it incorporates both the market method (based on the market-based royalty rates) and the income method (discount future savings), and the results are justifiable in both court and boardroom.

5 Key Steps in a Trademark Valuation Engagement

An effective trademark valuation is one that is done in a systematic manner. Some of the five major steps that the professionals need to know and implement irrespective of which among the trademark and brand valuation methods they are employing are listed below.

Step 1: Define the Purpose and Scope

When making valuation, it will always start by determining the reason why valuation is being made and what is being valued. Is it a licensing transaction, an acquisition or a law suit? Are the trademarks being valued as an independent property, or a larger brand portfolio? The purpose is what dictates the standard of value (fair value, fair market value and investment value) and affects all the other decisions that follow in the engagement.

Step 2: Understand the Brand’s Commercial Strength

As a valuation professional, one should be able to comprehend the brand qualitatively before implementing any numbers. In which markets does it operate? What is the customer loyalty strength? Is it a dominant market player or a niche player? Strong brand measurements usually have organized scoring systems that consider various aspects that include market leadership, brand knowledge, geographical coverage, and past investment. These qualitative scores make an impression on the quantitative assumptions of trademark valuation models.

Step 3: Isolate the Brand’s Economic Contribution

The profit of a company can be attributed to its trademark not all the time. The technology, its distribution network, its employees, and its processes are some of the things that make it some profits. The professional in valuation needs to ascertain the individual segment of economic value that is the flow of the brand. This can be normally done in a contributory analysis of assets, in which returns which can be credited to other assets are removed, and the remaining earnings are credited to the trademark itself.

Step 4: Forecast and Discount Future Brand Earnings

Having the earnings of the brand in isolation, the next thing is to project the earnings of the brand up to the remaining useful life of the brand and discount them to present value. The discount rate is supposed to be an indicator of the risk profile of the brand-specific cash flows, which is usually greater than the overall WACC of the company to reflect the particular risks associated with the intangible asset. This is the step where analytical ability is needed in depth since any minute variation in the growth rate assumptions or discount rates can produce a considerable effect on the end value.

Step 5: Sense-Check and Document the Findings

A good valuation is not confined to the spreadsheet. Findings must be compared with other approaches, benchmarked with similar transactions and sensitivity to major assumptions checked. There must be detailed documentation of assumptions, sources of data and methodology, especially where the valuation will be tested by auditors, regulating authorities or even a court. Documentation also produces a record which can be re-examined and amended as things evolve.

Real-World Examples and Lessons Learned

Real life dealings furnish some of the best examples of why brand and intellectual property valuation is important and how the procedures work in actual practice.

Take the example of the purchase of Kraft by Heinz in 2015. In the case of the merger when Heinz bought Kraft to form The Kraft Heinz Company, accountants under ASC 805, were expected to divide the purchase price on all the assets that were acquired including brand names. The valuation of the Kraft and Heinz trademarks was done independently on an income-based trademark and brand valuation method and billions of dollars were recognised as intangible assets on the balance sheet. A few years on Kraft Heinz had to record billions of goodwill and intangible asset values as being impaired to make a bitter lesson that brand value does not remain constant and needs to be reviewed whenever there is a change in market conditions, consumer trends and competitive forces.

The next teaching case is the example of the valuation of Coca-Cola brand. Interbrand and Brand Finance are among the brand consultancies that have continuously estimated the brand value of Coca-Cola to lie between US $70 billion and US $100 billion, based on the methodology. This difference in these estimates is indicative of the true complexity of brand and intellectual property valuation two reputable companies making slightly different assumptions with respect to royalty rates, growth projections and discount rates can arrive at materially different values. This highlights the necessity of being transparent in the methodology, as well as the necessity of professionals to be critically appraisive of the assumptions of any valuation.

The Apple vs Samsung case in the United States has been the dramatic example in regard to trademark valuation and the meeting of legal damages in the context of trademark litigation. Financial damages (that were inflicted by design and trademark infringement) were quantified on the basis of income-based models and market evidence using expert witnesses. The case demonstrated that trademark valuation is not simply an accounting task, it is a science that involves commercial judgment and legal knowledge and that it is necessary to be able to communicate complex financial analysis understandably to non-expert audiences.

Table 2: Comparison of Trademark and Brand Valuation Methods

| Method | Basis of Value | Best Used When | Key Limitation |

| Cost Approach | Brand equity How much it would cost to re-create the brand. | Brands that are young or newly established. | Lacks no market earning power. |

| Market Approach | Similar exchanges in the market. | Market with other brands of the same nature. | Similar data is not always available. |

| Income Approach (RfR) | Present value of royalty savings | Established brands; M&A; licensing | Sensitive to discount rate assumptions |

| Excess Earnings | Other assets less earnings. | Preeminent brand, M&A purchase price allocation. | Complex; involves contributory asset charges. |

Common Challenges in Brand and Intellectual Property Valuation

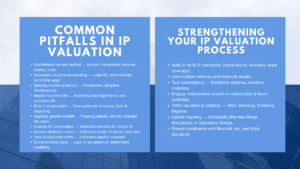

Although there are clearly developed trademark and brand valuation methods, practitioners are always faced with a number of challenges that are recurrent and demand judgment and experience coupled with close documentation.

Data availability is one of the greatest problems. Income method presupposes sound predictions of revenue on brands, standards of royalty rates, and discount rates. Practically, similar royalty rate data tend to be proprietary, transactional or are not directly comparable to the brand being estimated. There is a certain indication in such databases like RoyaltyStat or the ktMINE platform, but the choice and adaptation of comparables require the caution of the practitioners. Even an error of one or two percentage points in the calculation of the royalty The second issue is that brand value is no longer linked with the other intangible resources of the company like customer relations, technology, and goodwill. Most brands create value in part through the customer loyalty programmes they have, through proprietary formulas, or distribution arrangements. It is conceptually challenging and practically tasking to unwind the contribution of the trademark on these co-dependent assets. The brand and intellectual property valuation professionals should have a clear guideline on how they give the value between overlapping intangibles.

Lastly, is the issue of subjectivity and defensibility. In contrast to the situation with physical assets where market prices can be confirmed, brand valuation is a subject that depends on assumptions of future-related issues such as revenue growth, market share, consumer behaviour which are quite uncertain. This renders the process susceptible to challenge by auditors or taxation authorities or litigating counsel. Professionals should make sure that all assumptions made are evidence-based and that their practice complies with accepted standards including the International Valuation Standards (IVS) or the RICS Red Book which are starting to cover the valuation of intangible assets.

Process Flow 2: End-to-End Workflow of Brand Valuation Engagement

| Phase | Key Activities | Typical Duration |

| Scoping | Establish intent, criterion of value and scope; determine the requirements of data. | 1–2 days |

| Data Collection | College financial statements, royalty standards, market research, legal documents. | 1–2 weeks |

| Brand Strength Analysis | Mark the brand on qualitative factors; change royalty rate or discount rate. | 3–5 days |

| Valuation Modelling | Income build model; RfR or excess earnings, sensitivity analysis. | 1–2 weeks |

| Review & Challenge | Compare to other procedures; peer review; management discussion. | 3–5 days |

| Documentation & Reporting | Develop written report containing assumptions, working and conclusions. | 1 week |

The above table is representative of a mid-sized engagement. Huge cumbersome brand portfolios, especially those with different geographies and different trademark registrations, may require several months. The knowledge of this workflow will allow junior professionals to make realistic expectations and make a meaningful contribution to every stage.

Actionable Insights for Professionals

The art and science of measuring trademark and brand value is there. The valuation techniques of the trademark and brand discussed in the current article, that is, cost, market, and income, have their niche, and experienced professionals understand when and how to use all of them. The ability to make good commercial decisions, explain complicated results in a very clear manner and justify assumptions in a way, which can be openly criticized, is what makes great work in this area.

As a junior and mid-level professional aiming at developing the skills of trademark valuation and brand and intellectual property valuation, the following actionable steps will help develop at a rapid rate. To begin with, get a working knowledge of the three primary valuation methods and how each works: not just the formulae. Second, make use of actual data on transactions and published brand value ratings (like those of Interbrand or Brand Finance) to develop an intuitive sense of what makes the brand value in various industries. Third, go through the practice of creating financial models that isolate brand-driven earnings, and stress-test your assumptions in order to know which variables are most important to the value.

Fourth, work with the professional standards that exist within this space. Guidance on the valuation of intangible assets which is published by International Valuation Standards Council (IVSC) is more and more being referred to by courts, regulators and auditors around the globe. Being conversant with these standards represents professional credibility. Fifth, find out cross-functional experiences that integrate legal, financial and commercial views brand and intellectual property valuation is at the border of all three and those professionals who can cross-sell between these disciplines will be most effectively placed to add value.

Finally, due to increasing role of intangible assets in the global economy, trademark valuation will continue to play a significant role in the business decision-making. The current investors in the training of their knowledge of the trademark and brand valuation techniques are creating a skill base that will not grow obsolete, and will be in demand, in a few years.