Certified IP Valuation for Tax Planning

The Role of IP Valuation in Tax Planning and Transfer Pricing

Introduction to Certified IP Valuation for Tax Planning

Intellectual property (IP) has become one of the most valuable yet complex classes of assets in the global economy. In an era defined by innovation, data, and digitalization, companies derive significant portions of their enterprise value from intangible assets such as patents, trademarks, proprietary technology, and brand equity. As these assets cross borders through licensing, manufacturing arrangements, or intra-group services, their valuation takes on critical importance—not only for financial reporting but also for tax planning and transfer pricing.

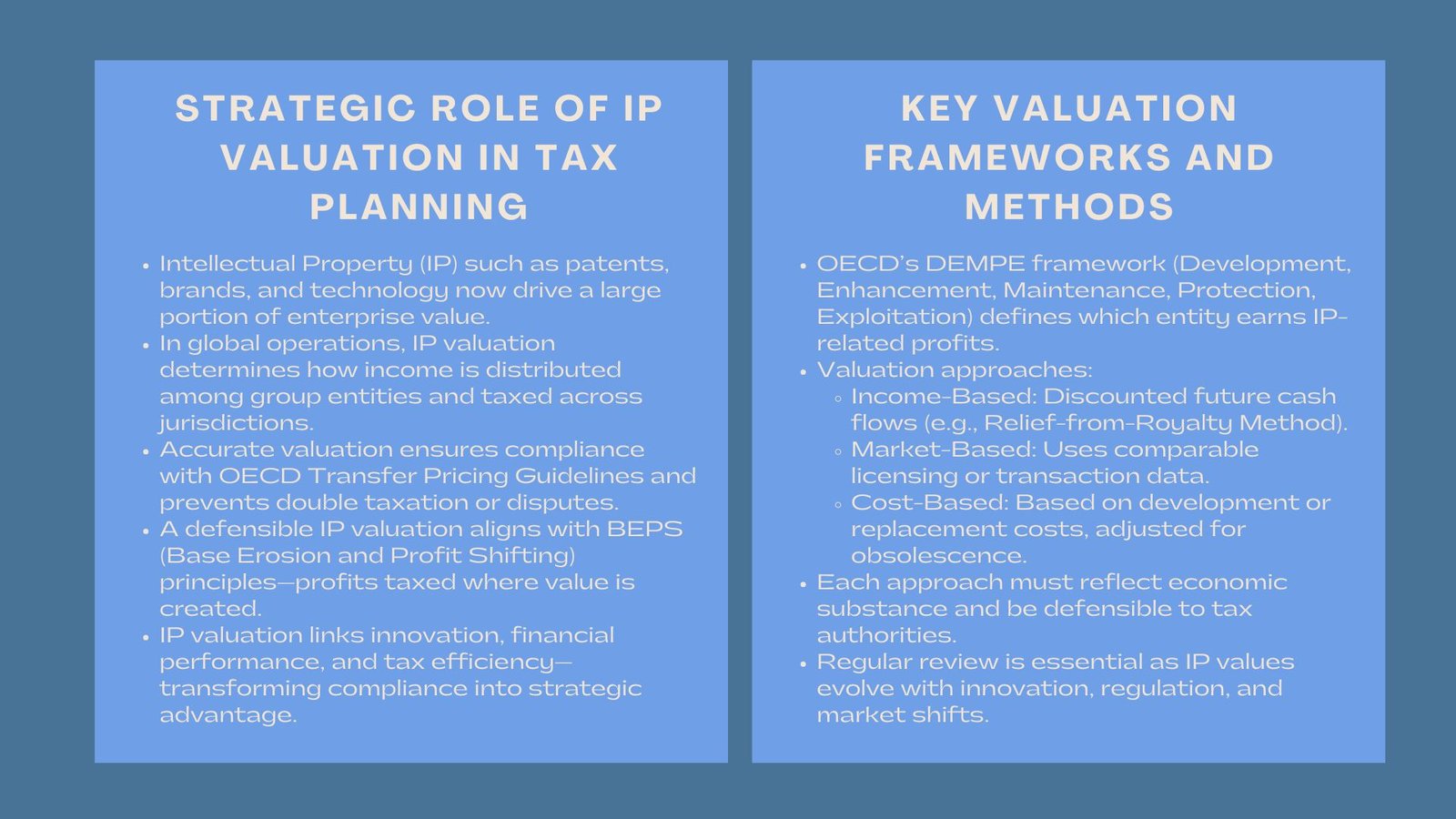

The valuation of IP determines how income is allocated among entities within a multinational group and how taxable profits are distributed across jurisdictions. Inappropriate or inconsistent IP valuations can lead to significant tax exposure, double taxation, or challenges from tax authorities. Conversely, a robust and defensible IP valuation strategy can optimize a company’s global tax efficiency while ensuring compliance with international regulations, including the OECD Transfer Pricing Guidelines and BEPS (Base Erosion and Profit Shifting) framework.

This article explores the conceptual underpinnings, valuation methodologies, and strategic significance of intellectual property valuation for transfer pricing compliance, emphasizing how it bridges legal compliance, corporate strategy, and financial performance.

The Relevance of IP Valuation in Modern Tax Strategy

Bridging Tax Compliance and Business Value

In globalized operations, IP valuation sits at the intersection of tax regulation and corporate strategy. Intellectual property is often developed in one jurisdiction but exploited across several others, through licensing agreements, royalties, or cost-sharing arrangements. For tax authorities, these transactions must occur at arm’s length—that is, the price charged between related entities must be equivalent to what would be agreed upon between independent parties.

Accurate IP valuation is therefore essential to determine appropriate transfer prices and to ensure that income is taxed where value is actually created. From a business perspective, it allows companies to structure their operations and intercompany agreements in a manner that reflects the true economic contribution of each entity. This alignment between compliance and value creation is the cornerstone of sound tax planning.

Responding to Regulatory Complexity

The increasing sophistication of intangible assets has made IP valuation a focal point for international tax authorities. The OECD’s BEPS Action Plan, particularly Actions 8–10, emphasizes that profits should align with economic substance and value creation. As a result, multinational enterprises (MNEs) must substantiate that their IP transfer prices are supported by credible valuation analyses, reflecting the functions performed, assets used, and risks assumed by each related entity.

This regulatory pressure means that valuation is not a one-time exercise but an ongoing process requiring periodic review and documentation. Failure to establish or defend an appropriate IP value can lead to adjustments, penalties, and reputational damage. Thus, IP valuation underpins both strategic tax efficiency and corporate compliance integrity.

Fundamental Concepts of IP Valuation in Tax and Transfer Pricing

Types of Intellectual Property Subject to Valuation

In tax and transfer pricing contexts, the term intellectual property encompasses a broad range of intangible assets, including patents, trademarks, trade secrets, software, databases, and marketing intangibles such as brand names and customer lists. These assets often drive revenue through royalties, license fees, or embedded profit margins.

However, not all IP has the same tax implications. For instance, technology-related IP (like software or patents) typically generates measurable cost savings or incremental profits, making it easier to value using income-based methods. Marketing intangibles, such as brands or customer relationships, are often valued using more judgmental approaches since their benefits are indirect and harder to isolate. Recognizing these distinctions is crucial in selecting appropriate valuation methodologies for transfer pricing purposes.

Valuation Principles under the OECD Guidelines

The OECD Transfer Pricing Guidelines provide the foundation for valuing IP within multinational groups. According to these guidelines, the value of IP should reflect its economic contribution, assessed through the DEMPE framework—Development, Enhancement, Maintenance, Protection, and Exploitation of intangibles. This framework identifies which entity performs key functions and bears related risks, thereby determining the share of profits attributable to each entity.

A sound IP valuation must consider who funded the R&D, who legally owns the IP, who manages the protection and exploitation of rights, and how risks are shared. The output of the valuation process informs intercompany pricing policies that must stand up to tax authority scrutiny.

Valuation Methodologies for Tax and Transfer Pricing

Income-Based Approach

The income-based approach is the most commonly used in IP valuation for tax and transfer pricing because it directly links the value of an asset to the future economic benefits it generates. This approach involves projecting the expected cash flows attributable to the IP and discounting them to their present value using a rate that reflects the risk of those cash flows.

A frequently applied model under this approach is the Relief-from-Royalty Method (RFRM), which estimates the value of IP by determining the hypothetical royalties a company would have to pay if it did not own the IP but instead licensed it from a third party. The resulting value represents the cost savings associated with ownership.

Another income-based technique is the Excess Earnings Method, which isolates the portion of profits attributable to IP after deducting returns for contributory assets such as fixed assets and working capital. Both models require robust assumptions regarding revenue forecasts, royalty rates, and discount rates, all of which must be defensible in tax audits.

Market-Based Approach

The market approach determines IP value by reference to comparable market transactions, such as licensing agreements or IP sales involving similar assets under comparable conditions. This approach is particularly useful when reliable market data exists, such as industry-standard royalty benchmarks.

However, in transfer pricing contexts, exact comparables are rare, given the unique nature of IP and confidentiality of licensing terms. Adjustments must therefore be made for differences in geography, exclusivity, asset maturity, and contract terms. Despite its limitations, the market approach provides valuable external validation for income-based results, enhancing the credibility of valuation conclusions.

Cost-Based Approach

The cost approach estimates IP value based on the cost of reproducing or replacing the asset, adjusted for obsolescence and functional depreciation. It is typically used for early-stage IP or internally developed technology where future benefits are uncertain. Although it provides a conservative baseline, it often understates the economic value of IP that yields ongoing or scalable benefits.

In tax planning, the cost approach may serve as a cross-check rather than a primary valuation method, particularly when income-based models are difficult to apply due to data constraints.

Integrating IP Valuation into Tax Planning

Structuring and Ownership Optimization

A key objective of tax planning is to ensure that IP is located and managed in jurisdictions that support both operational efficiency and favorable tax treatment. IP valuation plays a central role in determining which entity should own, license, or develop the IP. For example, companies may establish IP holding entities in countries offering innovation box regimes or R&D tax incentives, provided that the structure meets substance requirements.

Valuation ensures that any IP transfer between entities—such as from a development center to an IP holding company—is priced at fair market value. This prevents profit shifting accusations and aligns taxable income with actual value creation.

Intra-Group Transactions and Royalty Setting

When a subsidiary licenses IP from a related entity, the royalty rate must reflect an arm’s-length price. IP valuation provides the analytical foundation for setting these rates, considering comparable licensing transactions, expected profitability, and economic risk sharing.

A defensible valuation supports the transfer pricing documentation required by tax authorities, minimizing the risk of double taxation or adjustment. For multinational enterprises, establishing consistent royalty policies across jurisdictions enhances transparency and reduces administrative complexity.

Mergers, Acquisitions, and IP Migration

In the context of M&A or corporate restructuring, IP often changes ownership within the group or across borders. Accurate valuation ensures that these transfers are recorded at fair value for both tax and accounting purposes. For cross-border IP migrations, tax authorities typically require extensive valuation reports to justify the transfer price and prevent underpricing intended to shift profits.

Proper valuation also helps companies plan the tax consequences of IP disposal, such as capital gains recognition or deferred taxation under specific regimes. As a result, IP valuation serves as a critical component of due diligence, deal structuring, and post-acquisition integration.

Transfer Pricing Documentation and Compliance

The Importance of Defensibility

A well-documented IP valuation not only determines the transfer price but also serves as evidence of compliance in tax audits. Transfer pricing documentation must explain the valuation method applied, the rationale for selected assumptions, and the linkage between IP value and the DEMPE functions.

Tax authorities increasingly demand transparency on how IP-related income aligns with operational activities. Thus, valuation reports should incorporate both qualitative and quantitative analyses, demonstrating how intercompany transactions reflect economic substance rather than mere tax optimization.

Aligning with OECD and Local Requirements

While the OECD Guidelines provide the global framework, each jurisdiction may have additional rules governing IP valuation and transfer pricing. Companies must align their methodologies with local documentation standards, such as the Master File and Local File requirements, ensuring consistency across entities.

Moreover, regular re-evaluation of IP value is essential, especially when significant changes occur—such as product launches, regulatory shifts, or market disruptions—that may alter the IP’s economic potential. Continuous monitoring and periodic updates make valuations more resilient under scrutiny.

Technological Advancements and the Future of IP Valuation

Leveraging Data and Analytics

Modern valuation increasingly relies on data-driven insights. Predictive analytics and machine learning enable more accurate modeling of IP-related revenues, cost savings, and market comparables. These tools enhance the reliability of assumptions, reduce subjectivity, and improve the defensibility of transfer pricing positions.

For example, algorithmic benchmarking tools can scan thousands of licensing agreements to identify royalty ranges consistent with market behavior. Similarly, automated cash flow modeling systems allow real-time adjustment of valuation inputs to reflect evolving market data or regulatory developments.

Integration with Global Tax Technology Platforms

Many multinational enterprises are now integrating IP valuation models directly into their global tax management systems. This allows continuous tracking of IP performance, centralized documentation, and streamlined reporting. Integration reduces manual errors, enhances audit readiness, and ensures that transfer pricing policies remain aligned with economic realities across jurisdictions.

Benefits of Robust IP Valuation in Tax and Transfer Pricing

Enhancing Tax Efficiency

Accurate IP valuation allows companies to optimize tax structures while maintaining compliance. By pricing IP transactions at fair market value, businesses can allocate profits in proportion to real value creation, ensuring that tax benefits are achieved within legitimate frameworks.

Mitigating Compliance Risks

Comprehensive and well-documented valuations reduce the risk of disputes, penalties, and adjustments by tax authorities. They demonstrate due diligence and adherence to international best practices, thereby safeguarding corporate reputation and financial stability.

Supporting Strategic Decision-Making

Beyond compliance, IP valuation provides management with insights into the profitability and scalability of different intangible assets. Understanding which IP assets contribute most to value creation supports strategic decisions in R&D investment, licensing strategy, and portfolio optimization.

Conclusion

The role of IP valuation in tax planning and transfer pricing extends far beyond technical accounting—it is a strategic discipline that connects innovation, economics, and regulatory compliance. In a world where intangibles drive most of a company’s value, accurate and defensible IP valuation ensures that profits are aligned with substance, risks are properly managed, and tax strategies are both efficient and compliant.

As tax authorities intensify scrutiny under BEPS and OECD frameworks, the demand for transparent, data-backed, and methodologically sound IP valuations will only grow. For multinational enterprises, integrating valuation into their broader tax and strategic planning is no longer optional—it is a critical element of sustainable global operations.

By combining rigorous financial analysis, robust documentation, and technological innovation, how to value intellectual property for tax planning under OECD guidelines organizations can turn IP valuation into a source of both compliance confidence and strategic advantage in the complex landscape of international taxation.