IP Valuation for Financial Reporting Compliance

IP Valuation for Financial Reporting and Audit Compliance

Introduction to IP Valuation for Financial Reporting Compliance

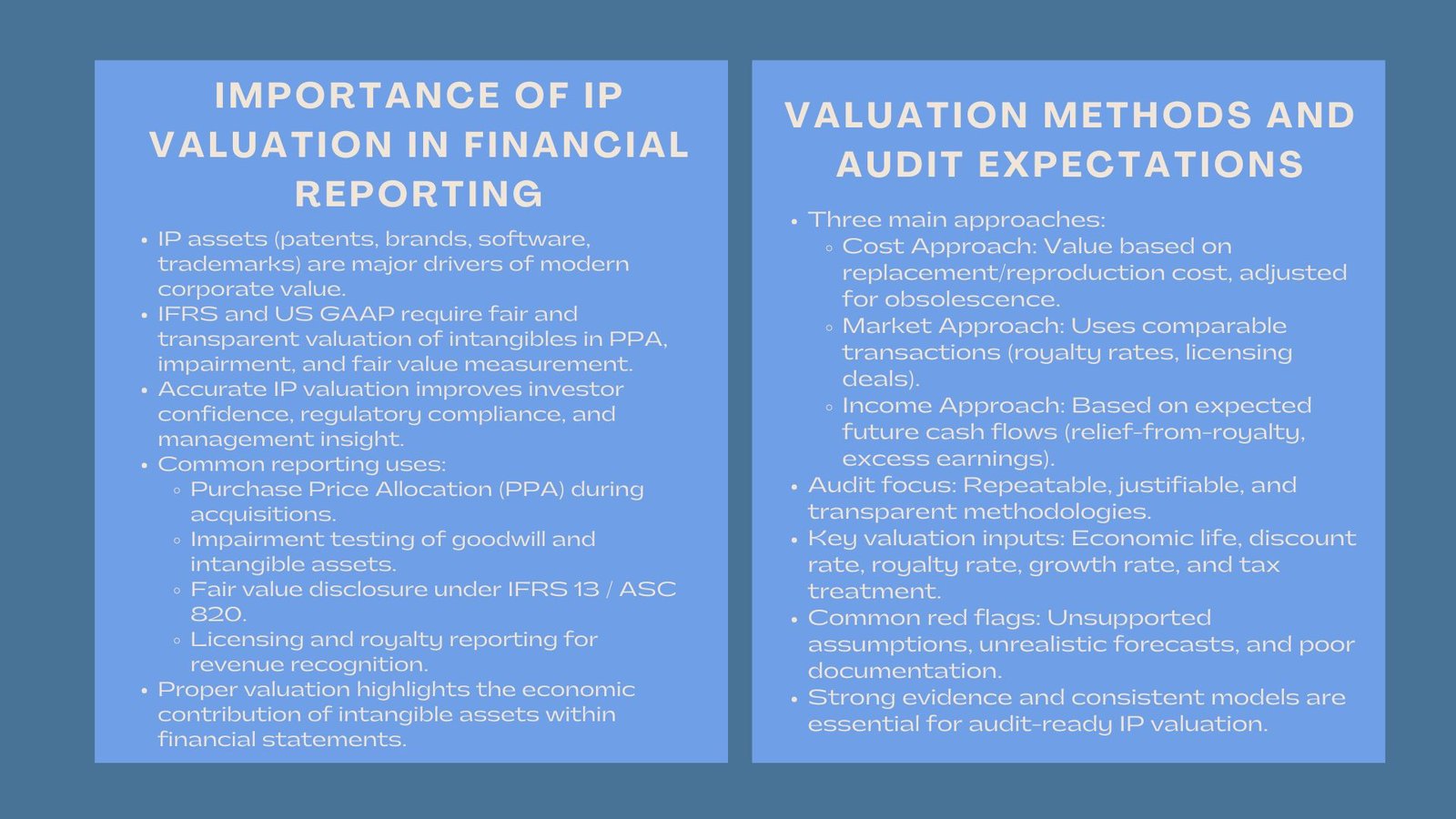

Patents, trademarks, software, and brands are intellectual property (IP) assets that are crucial in determining the competitive advantage of a company and its position in the market. With the growing dependence of the businesses on the intangible assets in creating value, the financial reporting standards have come to dictate efficient and transparent practices in measuring the intangible assets. Proper IP valuation is required not only to investors and the management but also to the auditors and regulators who are to verify the fair and compliant values are recorded in the financial statements. This paper discusses the integration of IP valuation with financial reporting and audit requirements, the major methodologies used and best practice of ensuring the maintenance of audit-ready documentation of valuation.The IP Valuation and Financial Reporting.

According to International Financial Reporting Standards (IFRS) and US Generally Accepted Accounting Principles (US GAAP), in certain situations intangible assets are required to be recognized and measured through business combinations, testing impairment, and transfer of assets. IP valuation assists in the fair valuation of these assets to be recognized and disclosed in the balance sheet accordingly. The most popular financial reporting purposes which involve the IP valuation include:- Purchase price allocation (PPA): Purchase in an acquisition Allocation of consideration paid in an acquisition to tangible and intangible assets, including identifiable IP.

- Impairment testing: It involves evaluating the carrying amount of an IP asset against the amount that may be recovered.

- Fair value measurement: This is a procedure that requires the determination of the market-based value of the IP assets that should be disclosed or transacted.

- Licensing and royalty reporting: This is to make sure that the revenue generated as a result of IP is recognized.

The Audit Perspective: Valuation Matters.

Another important use of auditors is to ensure that IP valuations are fair, justifiable and in line with the accounting standards. The audit procedure will entail the assessment of the valuation methodology, scrutiny of the major assumptions, and confirmation of whether fair value measurement is in accordance with either the IFRS 13 or ASC 820 concept of fair value. On the part of an auditor, the valuation should be:- Repeatable: With well-known and familiar methodologies.

- Justifiable: The evidence of market and documented assumptions.

- Clear: The connection between the financial reporting outcomes and the valuation drivers should be very clear.

Relevant Standards and Guidelines.

IP has a number of international standards that inform the way it has to be valued to comply with financial reporting and audits:- IFRS 3 – Business Combinations: Regulates the identification and fair value of the intangible assets acquired during the mergers or acquisitions.

- IAS 36 – Impairment of Assets: Obligates the annual impairment testing of the goodwill and indefinite-lived intangible assets.

- IAS 38 – Intangible Assets: Introduces the criteria of recognition, the models of intangible assets measurements, and the requirements of amortization.

- IFRS 13 – Fair Value Measurement: This standard gives a framework of measuring and disclosing fair value.

- IVS 210 and IVS 220 (International Valuation Standards): Provide technical instructions regarding the valuation of intangibles in a financial report.

Existing IP Valuation methods in Financial Reporting.

When calculating fair value of IP assets, valuation professionals normally use three acceptable methods, which include cost, market, and income methods. Both of them give alternative explanations regarding the contribution made by intangible assets to the enterprise value.Cost Approach: Replacement or Reproduction Value.

Cost method calculates the value using the cost of replacement of the utility of the asset. This involves the direct costs (development, labor, materials) and the indirect costs (management, testing, and overhead). Functional or economic obsolescence is adjusted. Although it offers a physical foundation, the cost method might not reflect the economic future or intangible cash flow of brand-based IP that can be created.Market Approach : Comparable Transaction Evidence.

The market approach based its value on the observed market dealings taking related IP assets. Comparable technologies or brands undergo comparison of the royalty rates, licensing agreements or M&A data by the analysts. This technique is particularly effective in the context of good market data, like in the case of the technology licensing or brand valuation. A relevant example is market-based IP valuation benchmarking for financial statement disclosures, where transaction comparables help support audit evidence for fair value estimates.Income Approach: Future Economic Benefits.

The income method is used to determine the value of the cash flows of the IP asset in the future which is expected to be gained. This method is the most widely applied in the financial reporting in that it represents anticipated returns which the intangible assets bring about the business. Strategies under this technique are:- Relief-from-royalty method: It is an estimation of the royalty that will be saved in lieu of owning the IP as opposed to licensing it.

- Excess earnings method: Determining the income that can only be attributed to the IP and then those returns are deducted as a result of other assets.

- Incremental cash flow approach: The comparison of the profits with the presence and absence of the IP asset.

Audit Ready Valuations Key Inputs and Assumptions.

In order to have audit compliance, all the assumptions in the valuation model should be clear and well-justified. Key elements include:- Economic life: The economic life is founded on market dynamics, legal protection and technological relevancy.

- Royalty rate or profit contribution: This is based on data available in the market or internal research.

- Discount rate: This is the indication that captures the risk profile, as well as the cash flow volatility of the IP.

- Growth rate: Within industry projections and management anticipations.

- Tax rate/ amortization: In line with financial statement policies.

Best Practices to Audit Compliance.

A compliant IP valuation based on audit requirements must provide methodological consistency, open assumptions and documentation. Key best practices include:- Prescription of methodologies in agreement with the IFRS and IVS standards.

- Recording every source of data, assumption and rationale.

- Multiple valuation methods should be used.

- Sensitivity testing to indicate the effect of critical assumptions on value.

- Making sure that forecasts and inputs are reviewed and approved by the management before submission to auditors.

Top Audit Problems and Auditing Solutions.

Auditors usually express their concern when IP valuations do not have enough supporting information or seem not to match the accounting guidance. Common challenges include:- Irregularity in the rate of discounts or royalties: Could not match the assumptions to the industry standards.

- Too positive estimates: Fail to align the management estimates with the market trends.

- Poor transparency: Inadequate record keeping of critical input.

- Mismatch of methods: Ineffective methods are applied to the kind of IP under valuation.

The Financial Reporting Strategic Value of IP.

In addition to compliance, IP valuation offers important information on the role of intangible assets in the performance of business. Monitoring the dynamics of IP value is important to the management to evaluate the brand strength, technology leadership, and results of innovation. It also facilitates strategic decision-making, whether it is licensing or divestment or the focus on R&D. Incorporation of valuation into financial planning and corporate governance will help organizations to clearly communicate to the investors and other regulators the power of intangible assets.Conclusion

The use of IP valuation in financial reporting is not just an accounting demand – it is a connector between innovation, strategy and transparency. It boosts the reliability of financial statements when performed based on the international standards and justifiable with the solid documentation, as well as provides the audit compliance. With the ever-increasing number of intangible resources that are taking over the contemporary balance sheets, any organization that has perfected the art of proper and audit-compliant IP valuation would benefit in a sustainable way in terms of investor trust and regulatory confidence.Frequently Asked Questions

Q1. What is IP valuation for financial reporting compliance?

IP valuation for financial reporting compliance is the process of determining the fair value of intellectual property assets such as patents, trademarks, software, copyrights, trade secrets, and proprietary technologies for inclusion in financial statements. The valuation helps organizations comply with accounting standards and ensures that intangible assets are reported accurately and transparently.

Q2. Why is IP valuation important for financial reporting?

Accurate IP valuation helps companies present a reliable picture of their financial position by properly recognizing, measuring, and disclosing intangible assets. It supports compliance with accounting standards, enhances transparency for investors and stakeholders, and provides a defensible basis for audits, mergers and acquisitions, impairment testing, and purchase price allocations.

Q3. Which accounting standards are relevant to IP valuation?

IP valuation for financial reporting commonly follows standards such as IFRS 13 Fair Value Measurement, IAS 38 Intangible Assets, and IFRS 3 Business Combinations. These standards provide guidance on the recognition, measurement, disclosure, and valuation of intangible assets and intellectual property in financial statements.

Q4. What valuation methods are commonly used for financial reporting purposes?

The three primary valuation approaches are the Income Approach, Market Approach, and Cost Approach. Depending on the nature of the intellectual property and the reporting objective, valuation professionals may apply techniques such as the Relief-from-Royalty Method, Multi-Period Excess Earnings Method (MPEEM), comparable transaction analysis, or replacement cost analysis.

Q5. How can businesses ensure their IP valuations are audit-ready?

Businesses can improve audit readiness by maintaining comprehensive documentation of valuation methodologies, assumptions, supporting data, financial forecasts, market research, legal ownership records, and valuation calculations. A strong audit trail allows auditors and regulators to verify the valuation process, review assumptions, and confirm compliance with applicable accounting and valuation standards.