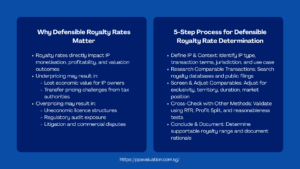

Defensible Royalty Rate Determination

Building Supportable, Evidence-Based Royalty Rates for IP Licensing, Valuation, and Transfer Pricing

Introduction to Defensible Royalty Rate Determination

The question of the appropriate royalty rate is one of the most impactful in the economics of intellectual property: What is the right royalty rate? The solution is of great essence. Too small, the IP owner misses out on monetising a valuable asset, or the owner risks a transfer pricing issue with tax authorities. If it is excessive, and the business model of the licensee becomes uneconomical, the licensing arrangement becomes a source of litigation, or the rate is found to be non-arm’s-length in a regulatory audit. A stepwise guide to defensible determination of royalty rates based on intellectual property assets is not merely a technical activity – it is a risk management discipline that is at the intersection of valuation, tax, and commercial strategy.

The title of this article has the word defensible, which has not been placed randomly. In most situations where the royalty rate is fixed, such as in brand licensing agreements, patent cross-licences, franchise agreements, or even in intercompany transfer pricing policies, the rate will at some point be subject to external scrutiny. In the United States, the United Kingdom, Australia, Germany, and throughout the Asia-Pacific, tax authorities challenge on a regular basis the royalty rates that they find to be inconsistent with the arm length standard. In a patent litigation proceeding, courts consider whether a royalty rate is one that would have been negotiated between a hypothetical willing licensor and a willing licensee. Auditors insist that royalties that were paid in the valuation of a brand or purchase price allocation must be supported by similar market data. A rate that cannot be justified by means of evidence and arguments is a rate that poses danger.

This article presents a practical, systematic guide to the determination of royalty rates for professionals in the fields of IP valuation, tax advisory, licensing practice or corporate finance. It describes the fundamental methodologies, the databases and data sources that support a credible analysis, the five steps followed by experienced practitioners, evidence of real-world cases of documented disputes and transactions, and the challenges that have most often arisen when setting rates without adopting sufficient rigour. Regardless of whether you are just starting your career or specializing in royalty rate analysis, this guide will offer you a framework that will enhance the quality and defensibility of your royalty rate analysis.

Why Defensible Royalty Rate Determination Must Be Based on Market Evidence

The arm length standard is the most vital conceptual basis in considering factors affecting defensible royalty rates in technology and brand trademark licensing. This principle, captured by Article 9 of the OECD Model Tax Convention and adopted by virtually all major tax jurisdictions, is that transactions between related parties should be priced as though they were conducted between independent parties, dealing at arm’s length in similar circumstances. In the case of royalty rates, this would mean the rate that would have been charged by a parent company to a subsidiary to use a trademark, or would have been charged by one group entity to another to use patented technology, should have reflected what would have been charged by an unrelated licensor to an unrelated licensee to use the same IP under similar conditions.

This standard appears simple in principle, but is in fact very hard to fulfill in practice, since analogous transactions of IP licensing are hardly ever perfectly analogous. Two pharmaceutical patent licences could entail the drugs in the same therapeutic area but at various phases of clinical development. Two brand licences can be in the same industry but with brands with radically different degrees of consumer awareness and price power. The task facing practitioners is to identify the most similar comparables available in market data and make principled, documented adjustments to the differences. The essence of defensible determination of royalty rates is the process of finding, screening, and adjusting comparables.

The evidence bar has increased a lot in the last ten years. The OECD tax authorities have spent a lot of money to create their own IP transactions database and create specialist transfer pricing teams with IP knowledge. A number of leading jurisdictions have introduced new mandatory country-by-country reporting and documentation requirements that allow authorities to more easily identify royalty rates that seem to be inconsistent with market standards. Meanwhile, courts in intellectual property cases have criticized mechanical rate-setting policies, most especially the long-since discredited so-called 25 percent rule of thumb, instead of pursuing more rigorous, evidence-based analyses. Those professionals who comprehend this setting and model their royalty rate studies in ways that reflect that comprehension are much better placed to stand scrutiny.

Defensible Royalty Rate Determination Core Methodologies

The three main analytical tools that are used in the application of the Relief from Royalty (RfR) method on the valuation of intangible assets and in the licensing and other royalty rate determination environments are based on three main complementary analytical tools: the Comparable Uncontrolled Transaction (CUT) method, the Relief from Royalty (RfR) method, and the Profit Split approach. Each of them possesses its own logic, data needs, and scenarios of the best fit.

The CUT technique looks to find licensing agreements between unrelated parties that involve IP that is sufficiently similar to the IP being valued or priced. These deals are sourced from commercial databases like RoyaltySource, ktMINE, and the Orbis IP of Bureau van Dijk, as well as publications such as the court decision in the intellectual property litigation. The advantage of the CUT method is that it is based on actual market transactions; its disadvantage is that, indeed, similar transactions are hard to find, and the adjustments that need to be made to reflect the differences in the IP type, exclusivity, territory, and duration can be extensive and subjective.

The Relief from Royalty technique is a rate-derivation technique, as well as a valuation technique. As a valuation approach, it values an IP asset by capitalising the royalty stream that is not notionally paid by the owner of the IP property, but by virtue of the owner being the owner of the IP. The royalty rate is applied to a forecast revenue base whereby the resulting annual royalty savings are tax-effected and the resulting post-tax savings stream is discounted to a present value using an appropriate discount rate. The output is the IP’s value. Yet the technique also works in reverse, in that, when the goal is to determine a rate, not a value, the practitioner identifies the rate, which, when applied to the revenue base, will result in a capitalised royalty stream that is consistent with the independently assessed value of the IP. This dual-purpose application of the Relief from Royalty approach to intangible asset valuation and licensing the Relief from Royalty approach to intangible asset valuation and licensing in this dual-purpose way is one of the most powerful weapons in the IP practitioner’s arsenal, because it provides an internal consistency check: the rate and the value are derived using the same analytical framework, and must be mutually coherent.

| Framework / Factor Set | Core Logic | Current Acceptance in Practice |

|---|---|---|

| 25% Rule of Thumb | Licensor gets 25% of the operating profit attributable to the IP, and the licensee gets the remaining 75%. | The courts of the US have said that it is not a starting point at all (Uniloc v. Microsoft, 2011); it is still used informally as a sanity check. |

| Georgia-Pacific Factors (US Patent) | 15 qualitative and quantitative variables to decide on a hypothetical negotiated royalty in patent disputes. | Normal in patent litigation in the US; powerful in the transfer pricing and licensing practice worldwide. |

| Relief from Royalty (RfR) | Royalty rate on estimated revenue; the resulting royalty stream, discounted to the present value of the stream, gives the value of the asset and the rate at the same time. | The main tool of IP valuation under IFRS 13, OECD TP guidelines and most IP litigation situations all over the world. |

| Profit Split Approach | The amount of profit gained as a result of the use of IP is split between the licensor and the licensee in proportion to their relative contribution. | Applied in situations where the parties have distinct and valuable functions to perform; OECD BEPS guidance includes embedded. |

Table 1: Frameworks Used in Defensible Royalty Rate Determination

Step-by-Step Process for Defensible Royalty Rate Determination

The step-by-step guide to defensible determination of royalty rates through the application of intellectual property assets that have been practised by experienced practitioners in licensing, valuation, as well as transfer pricing engagements can be broken down into five core steps. Both of them demand technical expertise as well as commercial acumen.

Step 1: Identify the IP Asset, the Transaction, and the Analytical Context.

The practitioner needs to come up with an accurate view of the IP asset itself and the situation in which the royalty rate will be applied. This involves determining the legal form of the IP (patent, trademark, trade secret, software licence, know-how), its economic characteristics (what revenue or profit stream does it make possible?), the scope of the licence (exclusive or non-exclusive, territorial limits, field of use restrictions, duration), and the regulatory or commercial purpose the rate will serve (transfer pricing compliance, third-party licensing negotiation, IP valuation for financial reporting, litigation support). All these dimensions influence what similar transactions are applicable and what changes will have to be made. A royalty rate imposed on a transfer pricing intercompany licence in one of the many competitive consumer goods markets will require a different analytical method from that which is used in a patent cross-licence in a technology standard-setting environment.

Step 2: Scan Databases and Find Potential Comparables.

The next thing is to look in the existing databases of third-party licensing transactions and find possible comparables with the IP and transaction. This is where the factors that have to be put into operation in search criteria to attain defensible royalty rates in technology and brand trademark licensing. In the case of technology IP, the relevant search parameters will be the technology field (with IPC or CPC patent classification codes where applicable), the level of commercialisation, the product type generating the royalty, as well as whether the licence is exclusive. In the case of brand trademarks, the parameters of relevance include the industry sector, the geographical coverage of the licence, the market position and recognition level of the brand, and whether the licence is a master brand or a sub-brand arrangement. The searches of databases should be recorded in detail, including the search terms used, the number of results returned at each level of the filter, and the criteria used to decide the results to keep at each step of the search. This is a document that is vital should the rate later be disputed.

Screen and Adjust Comparables of Differences: Step 3.

The crude product of a database query virtually always needs a significant amount of screening and refinement to allow it to be used to draw a rate conclusion. Qualitative is the initial stage of the screening: to isolate the transactions that reflect materially different IP types, dramatically different market positions, or unusual commercial terms that would make them unreliable benchmarks. The remaining transactions in turn demand quantitative adjustment to differences in exclusivity (exclusive licences fetch higher rates compared to short-term ones), territorial scope (global licences versus single-country licences), duration (longer licences may have different rate patterns than shorter ones), and the business relationship between the parties (arm-length transactions between natural competitors versus ones between complementary businesses). The most prevalent source of difficulty in regulatory audit and litigation is each adjustment being documented and justified, with unexplained or mechanically applied adjustments being the most common sources of challenge in regulatory audit and litigation proceedings.

Step 4: Compare with other Methods and Reasonableness Tests.

The conclusion of a royalty rate based on one analytical method is inherently less defensible than one that is supported by a variety of methods. After the CUT-based rate range has been determined, it should be compared with at least one other method. The Profit Split approach requires answering the question of whether the proposed rate is in line with a commercially reasonable apportionment of the profit resulting from the licensed IP between licensor and licensee. In the case where the rate charged leaves the licensee with less profit than it needs to run its own operations and make a market return on its tangible resources, as well as its routine operations. In case the implied compensation to the licensor on the IP is extremely lower than what can be achieved by a self-owned IP in the market, the rate might be too low. Another reasonableness test based on the Relief from Royalty method checks that the capitalised royalty stream at the proposed rate has an IP value that is consistent with the independently determined value of the asset. In case the result of these checks materially differs, the difference must be examined and eliminated prior to a rate being determined.

Step 5: Finalize on the Supportable Range and record the Reason.

The result of a defendable determination of royalty rate is not a single point estimate but rather an arm’s length range or a central point of the range that is indicative of the weight of the evidence. The range should be recorded in a written memorandum or report, explaining the IP under analysis, the circumstances of the transaction, the databases searched and how, the similar transactions that were selected and the reasons, the adjustments made and their basis, the cross-checks made and the conclusion, all of which should be documented. The main defence against challenge is that such a rate analysis is well documented, logically structured, and presented in an evidentiary manner. In the case of professionals operating under the requirements of transfer pricing documentation, e.g., the requirements of OECD BEPS Action 13, this documentation also has its formal legal status and must correspond to some specific content requirements. It is as important to complete the step-by-step guide of a well-structured, written conclusion to the analysis as the analysis itself.

Step-by-Step Royalty Rate Determination Process

| Define IP & Context Asset type, use, jurisdiction, term | ▶ | Database Research RoyaltySource, ktMINE, SEC filings | ▶ | Screen & Adjust Comps Filter by relevance; apply adjustments | ▶ | Cross-Check Methods 25% rule, profit split, relief from royalty | ▶ | Conclude & Document Supportable range; rationale memo |

Process Flow 1: End-to-End Royalty Rate Determination Workflow

Relief from Royalty Valuation Workflow

| Project Revenue Base Forecast revenue attributable to IP | ▶ | Apply Royalty Rate Benchmarked rate × revenue = royalty stream | ▶ | Tax-Effect Royalties Post-tax royalty savings computed | ▶ | Discount to PV Apply IP-specific discount rate / WACC | ▶ | IP Value Output Capitalised royalty savings = brand / IP value |

Process Flow 2: Applying the Relief from Royalty Method to Derive IP Value and Cross-Check Rate

| IP / Asset Type | Typical Rate Range | Royalty Base | Key Rate Drivers |

|---|---|---|---|

| Pharmaceutical patents | 2%–10% of net sales | Net sales revenue | Development stage, exclusivity, clinical risk persisting. |

| Software / SaaS technology | 5%–15% of revenue | Licence or subscription revenue | Embeddedness, switching cost, open source alternatives. |

| Consumer brand trademarks | 1%–5% of net sales | Net sales revenue | Brand awareness, higher price, geographical coverage, and customer loyalty information. |

| Industrial/mechanical patents | 0.5%–3% of revenue | Product revenue | Technical differentiation, ease of design-around, standard-essential vs. non-essential. |

| Franchise/master brand | 2%–6% of gross sales | Gross franchisee sales | Intensity of system support, brand equity, territory exclusivity, and growth stage. |

Table 2: Royalty Rate Benchmarks for Different Intellectual Property Asset Types

Real-World Cases Demonstrating Defensible Royalty Rate Determination

A review of recorded conflicts and dealings where the determination of royalty rates was the focus of intense scrutiny offers the most practical lessons of what makes a rate really justifiable when put to the test. The view of the factors of influence on defensible royalty rates in technology and licensing of brand trademarks becomes even clearer when the lens of cases of inadequate analysis that resulted in costly outcomes is put in perspective.

The long-running dispute between the Australian Tax Office and a major US multinational distribution subsidiary in Australia, which paid royalties to an offshore IP holding company to use brand trademarks and marketing intangibles, is one of the most cited cases in the practice of transfer pricing and IP royalty. The issue that the ATO was grappling with was whether the rate of royalty as charged has remained an arm’s-length rate over the years as market conditions continued to change. The tax authority suggested that the increasing scale of operations and market position of the Australian subsidiary should have been reflected in a renegotiated and lower royalty rate, since a more profitable licensee with greater bargaining power would not have accepted the original terms unchanged. The case reaffirmed a very fundamental lesson, that royalty rates in intercompany arrangements are not fixed in stone, but rather should be reviewed on a regular basis, in order to ensure that they remain constant with the current arm’s length conditions, as well as the very process of the review should be documented.

The ruling of the US Federal Circuit in Uniloc USA v. Microsoft Corporation in 2011 essentially redefined the approach that the courts take to evidence of royalty rates. The court refused to accept the use of the 25 percent rule of thumb as a starting point in the reasonable royalty analysis by Uniloc because it was not based on the facts of the particular case. That ruling essentially put an end to the 25% rule as a litigation tool and highlighted that any proposed royalty rate ought to be based on the economic realities of the particular patent, the particular products in question, and the particular market environment. To practitioners who have practiced using the Relief from Royalty method of intangible asset valuation and licensing, the Uniloc decision is a reminder that methodological rigour is not an option–courts and regulators expect analyses that tie the proposed rate to observable market evidence that is specific to the IP in question.

A third educative case is on the franchise industry, where a UK-based quick-service restaurant chain wanted to know the royalty rate to be charged under its master franchise agreement with a sub-franchisee in a new European market. Instead of just using the internal rates of return of other markets, the advisers of the franchisor conducted a systematic search of comparable transactions using disclosed franchise disclosure documents (FDDs) of other restaurant brands operating in the target market. The analysis gave a range of rates between 3% and 5% of gross sales, with the central point of the rate informed by the brand’s above-average recognition scores in the target market compared to a similar set. This methodology, which involved a combination of database research and market-specific consumer recognition information, resulted in a rate that was accepted by the sub-franchisee as a commercially reasonable rate and which ultimately passed a regulatory test by the local competition authority. The moral of the story is that such comparability assessment is to be based on all the available evidence relating to the market position of the particular IP, rather than being generic sector benchmarks.

Common Challenges in Defensible Royalty Rate Determination

The real-life implementation of a step-by-step guide to defensible determination of royalty rates on intellectual property assets always presents a combination of issues that can only be effectively resolved by using a combination of technical expertise and professional judgement.

The most common practical challenge that is often faced is database constraints. The commercial databases like RoyaltySource and ktMINE collect disclosed licensing transactions based on public filings, judicial decisions, and reported deal information, but their coverage is not even across sectors and geographies. They are usually underrepresented in transactions in the specialised technology fields, early licences of pharmaceuticals, or markets other than those of North America and Western Europe. When the analogous set is thin–three or four transactions instead of ten or twenty–each analogous bears disproportional weight, and the adjustments which must be made to explain the differences between the analogues and the subject transaction become more substantial and more contentious. The effective mitigation is to search the database more broadly than the ideal comparable criteria would indicate, use the broad set of results to set the outer bounds of a reasonable range, and then make principled adjustments to tighten around the central estimate. It is vital to make this process transparent, i.e., display the whole search results, and explain why some transactions have not been included, to make it defensible.

The second problem is the interaction between the determination of the royalty rate and IP valuation, especially when the Relief from Royalty method is used to determine the valuation of intangible assets and licensing in financial reporting. The RfR approach considers the royalty rate to derive the value of the IP, but the royalty rate is not derived by back-solving a desired value, but rather by using it as the basis by which the value of the IP is derived. When practitioners permit the outcome they want concerning valuation to have a circular and indefensible impact on royalty rate assumption, they produce analyses that are circular and indefensible. The protection is to have the royalty rate range determined by CUT analysis prior to the construction of the RfR model, and to treat the value output of the RfR as an end in itself to be verified by independent value indicators as opposed to a value to be engineered.

The third issue is to maintain the current rates in the fast-evolving competitive business world. A royalty rate that was established on a technology platform five years ago may not reflect the current competitive position of the technology platform, the existence of open-source substitutes, or the change in the balance of bargaining power between licensor and licensee as the technology has developed. To facilitate transfer pricing, under the OECD guidance, it is clear that intercompany arrangements should be reviewed periodically, and where material changes in circumstances occur, they must be updated to reflect the current arm’s-length circumstances. To practitioners with long-term licensing portfolio management to-do-lists, whether as in-house IP counsel, tax managers, external advisers, etc., it is a best practice risk management and an increasingly explicit regulatory expectation.

Practical Takeaways for IP Valuation, Tax, and Licensing Professionals

One of the technically most challenging and commercially most significant issues in the intellectual property practice is the determination of royalty rates. The step-by-step guide to defensible determination of royalty rates as applied to intellectual property assets presented in this article, such as defining the IP and context, searching databases, screening and adjusting comparables, cross-checking with alternative methods, and concluding with documented rationale, furnishes a framework that yields rates that can withstand regulatory audit, litigation scrutiny, as well as commercial negotiation pressure. The framework is not an assurance of having a certain outcome, but it is a procedure on how to get to a result that can be described, justified, and defended.

The most practical beginning point for professionals in their early career is to become familiar, through practical experience, with the most important royalty rate databases and to practice the process of comparability assessment. The creation of the market knowledge that constitutes the comparability judgements that get more intuitive as time goes by is created by reading disclosure in licensing agreements in public filings, SEC 10-K filings in the United States, prospectus documents in equity markets, and published court decisions in patent litigation, which builds the market knowledge that makes comparability judgements more intuitive as time goes by. Having the analytical fluency necessary to answer the question: Understanding the structure of a Relief from Royalty model well enough to construct one on your own, and stress-test its behavior to changes in the royalty rate assumption, develops the analytical fluency difference between a junior professional who adds genuine value and a junior professional who is only able to execute instructions.

In the case of more senior practitioners, the priority insight of the cases and challenges encountered during the course of this article is the criticality of documentation and consistency of the processes. An internally rigorous but poorly documented rate analysis is almost as difficult to challenge as a poorly analysed rate analysis. The regulators, courts, and counterparties do not credit work which they cannot observe. It is the laying down in writing, in simple, well-constructed, written form, at every step of the process, not only at the very end of it, that it is laid down in writing which turns a technically sound analysis into a genuinely defensible one. The ability to use the Relief from Royalty method of valuing intangible assets and licensing and the wider royalty rate determination instrumentation is, finally, the type of expertise that gives rise to long-term professional credibility in IP valuation, tax advisory, and licensing practice.