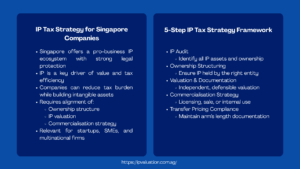

IP Tax Strategy for SG Companies

A Practical Reference for Tax, Finance, and Strategy Professionals

Introduction to IP Tax Strategy for SG Companies

For decades, Singapore has cultivated one of the most strategic and company-friendly IP cultures. From strong patent and trademark law to a range of incentives to promote the creation, retention and exploitation of IP on the island, Singapore views IP as a vital economic imperative. In this climate, companies from burgeoning tech start-ups to longstanding small and medium enterprises looking for new opportunities to boost revenues need to understand how IP can fit into their tax strategies. Singapore IP tax incentives for tech startups and expanding companies have opened up the possibility to lower the overall tax burden while creating valuable commercial assets.

However, the gap between IP assets and maximising their tax benefits is larger than one might think. IP needs to be properly owned by the right entity, valued in a way that is satisfactory to the Inland Revenue Authority of Singapore (IRAS) and any relevant grant administrators, and monetised in a way that is acceptable to IRAS and meets arm’s length and substance tests. It’s becoming increasingly useful for finance, tax, law, and strategy professionals to have a basic understanding of this landscape, whether you are an advisor to client companies, supporting the corporate tax function, or preparing to join a corporate finance team.

This article offers a step-by-step approach to IP tax strategies for Singapore companies. It explains key incentive schemes, the tax recognised methods of valuation, the paths to commercialisation and the tax implications of these, case studies with lessons for SMEs and growth companies, and the challenges that companies face in implementing these strategies. It offers practical takeaways for practitioners of all levels.

IP Tax Strategy for SG Companies: Singapore IP Tax Incentives

The simplest way to understand Singapore IP tax incentives for tech startups and other eligible companies is to outline the major schemes administered by the Inland Revenue Authority of Singapore (IRAS), the Economic Development Board (EDB), and EnterpriseSG. The three administer most of Singapore’s IP tax incentives, and they all apply to a distinct phase in the lifecycle of IP – development, acquisition, commercialisation, and income generation.

The IP Development Incentive (IDI) is the key income-based incentive for IP-developing companies with substantial activities in Singapore. The IDI allows income derived from the exploitation of approved IP assets – including royalties, licence fees and income in respect of the sale of goods containing approved IP – to be subject to a concessionary tax rate, instead of the 17% corporate tax rate. The IDI is based on the internationally accepted “nexus approach,” which ties the tax concession to the amount of R&D qualifying expenditure incurred in Singapore. This ensures that companies can’t simply place IP in Singapore without a local presence and expect to receive the concessionary rate.

For those who acquire rather than create IP, the Writing-Down Allowance (WDA) provides a way to claim an amortisation expense of the capital cost of acquiring qualifying IP (patents, trademarks, copyrights, registered designs, and know-how) over 5 or 10 years. This is especially important for companies that engage in acquisitions and carve-outs that include a substantial IP component. The enhanced R&D deductions under the Income Tax Act (Sections 14C, 14D, and 14E) also complement these tax incentives, enabling certain companies to claim 150% to 250% deductions on qualifying R&D expenses and substantially reduce the net after-tax cost of developing an IP portfolio. The key incentives for companies contemplating Singapore IP tax incentives for tech startups and SMEs are summarised in Table 1 below.

| Incentive / Scheme | Administering Body | Key Benefit | Who Qualifies |

|---|---|---|---|

| IP Development Incentive (IDI) | EDB | Lower tax rate on IP income | Companies that create IP with significant activity in SG |

| Writing-Down Allowance (WDA) for IP | IRAS | 5- or 10-year write-off for capital cost of acquired IP | Companies that acquire qualifying IP for use |

| Research & Development (R&D) Tax Deductions (Sections 14C/14D/14E) | IRAS | Increased deduction (150% – 250%) for R&D expenditure | Companies engaged in qualifying R&D in SG |

| Enterprise Development Grant (EDG) – IP component | EnterpriseSG | Up to 50% funding for IP strategy projects | SG-incorporated SMEs with 30% local shareholding |

| Pioneer / Development & Expansion Incentive (DEI) | EDB | Tax rate reduction (5% – 15%) for income | Companies with substantial new / enhanced economic activity |

Table 1: Singapore IP Tax Incentives for SG Companies – Schemes, Benefits, and Eligibility Criteria

How to Value Intellectual Property for Tax Planning in SG for Effective IP Tax Strategy

Knowledge of how to value intellectual property for tax planning in SG is among the most complex aspects of IP tax planning – and one of the areas in which practitioners and in-house teams run into the most trouble when providing advice to clients or colleagues. IP valuations for tax are not just performed using a single approach, but instead involve a selection from a number of accepted approaches, suitable to different scenarios and each with different levels of persuasiveness to IRAS and other tax authorities.

By far the most common method used to value IP in Singapore is the income-based approach, and in particular, the Relief from Royalty approach. This approach values the IP as the present value of the royalties that a company would pay to license the IP if it did not own it. This method is especially suitable for IDI claims and intercompany IP licensing, as it results in a value that is connected to the income potential of the IP. IRAS and transfer pricing advisers like this approach because the royalty rate benchmarks can be compared to actual market transactions, limiting the opportunities for manipulation.

The cost approach adds up the cost of developing or acquiring the IP, such as the salaries, materials, legal and registration fees, and other costs of R&D. Although easy to defend, it will generally underestimate the value of IP that is commercially developed because it fails to consider the value that markets would place on the earnings stream generated by the IP. The cost approach is, however, a good starting point for early-stage, pre-revenue companies that are seeking WDA exemption or government grants. See the table below for a comparison of key approaches to how to value intellectual property for tax planning in SG.

| Method | How It Works | Best Applied To | Tax Context Relevance |

|---|---|---|---|

| Income / Relief from Royalty | Calculates the royalties the company would have to pay if it licensed the IP | Patents, trademarks, with licensable income | WDA claims, IP transfer pricing, IDI qualification |

| Cost Approach | Sum of past R&D, legal, and registration expenses | Stage 1 IP without revenue | R&D deduction support, application for grants |

| Market / Comparable Transactions | Compared to other IP transactions | IP assets with comparable transactions | Arm’s length pricing, IP carve-outs in M&A transactions |

| Multi-Period Excess Earnings (MPEEM) | Bases the income on the IP asset only | Core IP assets leading the business value | IDI applications, intercompany IP licensing arrangements |

Table 2: IP Valuation Methods for Tax Planning in SG – Approaches, Use Cases, and Tax Relevance

5 Steps to Build a Tax-Efficient IP Structure

Developing a strategy for Singapore SMEs and growth companies on the tax impact of IP commercialisation needs to be systematic. The five steps below are a general guide that can be used by professionals when consulting clients or helping to manage an internal strategy exercise.

Step 1: IP Audit

The company needs to know what IP it has, or uses, before it can plan its tax strategy. A typical company, especially one in the rapidly growing tech sector, has IP assets all over the place: code written by the company’s software programmers, trademarks registered in different countries, customer databases, trade secrets such as algorithms and process knowledge that has not been previously identified or valued. An IP audit identifies all these assets, their legal ownership, and commercial and tax significance. When SMEs do this for the first time, they often find IP assets that are not legally owned by the Singapore entity that operates their business (such as IP that was developed by a founder prior to the company being incorporated and which has not been formally transferred to the company; or software developed with an overseas contractor who has not explicitly transferred the IP to the Singapore entity).

Step 2: Confirm IP is owned by the Right Entity

In Singapore, tax incentives are available only to the entity that owns the IP and engages in qualified activities in relation to the IP. If the IP is held in an offshore entity and the Singapore entity only uses the IP under a licence, then the Singapore company won’t be able to claim IDI rates or WDA on it. So structure is important. For multinational companies, the choice of where to hold IP is a trade-off between the Singapore tax benefits and transfer pricing and substance rules, as well as the reality of where R&D work is done. IRAS is vigilant to arrangements that seem to be aimed solely at transferring IP to Singapore without real substance, and the IDI’s nexus test is aimed at avoiding this problem.

Step 3: Obtain and Document an Independent IP Valuation

A documented independent valuation is required for most substantive IP tax planning transactions, such as applying for IDI, claiming WDA for an acquired IP asset, determining intercompany IP royalty rates, and documenting an IP contribution to a newly-established entity. The question of how to value intellectual property for tax planning in SG is thus not only academic, but practical and risk management-oriented. The valuation must be prepared at the time of the transaction or application, by an independent, qualified valuer and justified by a defensible set of assumptions. Those who rely on self-prepared valuations or simple rule-of-thumb calculations of royalty rates for determining the value of IP risks are challenged by IRAS and are exposed to adjustment, penalty, and reputational damage.

Step 4: Optimise Commercialisation from a Tax Perspective

IP commercialisation for Singapore SMEs has different tax consequences when the IP is commercialised via internal use, licensing to third parties, intercompany licensing to related entities or sale. The methods have varying tax implications for income recognition, withholding tax, and transfer pricing. Licensing income from foreign licensees could be subject to withholding tax in the foreign country, which needs to be planned for using Singapore’s broad network of double tax agreements. Capital gains on IP sales are exempt from Singapore tax, but IRAS will use substance-over-form analysis to determine whether an IP sale is a true capital gain or income in disguise, so IP sale transactions should be well-documented.

Step 5: Keep Transfer Pricing Documentation Up-To-Date

For companies with related-party IP transactions, such as intercompany licensing, shared services (including IP services) agreements, or IP assignment to group entities, compliance with transfer pricing is mandatory. IRAS expects related-party transactions to be carried out at arm’s length, with documentation to support the arm’s length price being maintained. Firms with related-party IP income or expenses of more than S$15 million per financial year face the transfer pricing documentation requirements in the IRAS Transfer Pricing Guidelines. While not strictly required for companies below this threshold, good documentation certainly minimises the risk of adjustment in an audit.

IP Tax Planning Process: End-to-End Flow

| IP Identification & Audit Map all IP assets owned or used | ▶ | Ownership & Structure Review Legal entity holds the correct IP | ▶ | Valuation & Documentation Independent valuation report | ▶ | Incentive Application IDI, WDA, R&D deductions filed | ▶ | Ongoing Compliance Annual review, TP documentation |

Process Flow 1: IP Tax Strategy for SG Companies: End-to-End IP Tax Planning Process Flow

IP Commercialisation Tax Pathway

| IP Created / Acquired In a Singapore entity | ▶ | Commercialisation Route License, sale, internal use | ▶ | Revenue Recognition Royalties, fees, capital gains | ▶ | Tax Treatment Applied IDI rate, WDA, deductions | ▶ | Transfer Pricing Check Arm’s length if cross-border |

Process Flow 2: IP Commercialisation Tax Pathway in Singapore: From IP Creation to Tax Treatment

IP Tax Strategy Case Studies: Lessons for Singapore SMEs and Growth Companies

Looking at the ways in which companies have dealt with the tax issues associated with the commercialisation of IP for Singapore SMEs and growth companies in recent years offers some of the best lessons. The following cases are examples of reported industry trends and advisor experience.

Take, for example, a UK-based cybersecurity firm that established its APAC operations in Singapore in the early 2010s. Against initial plans to establish a local sales and marketing arm, the company’s tax advisers arranged for the Singapore entity to own the APAC-specific software variants and customer data models that were developed by the Singapore engineering team. By taking steps to ensure that the IP development was actually carried out in Singapore (local staff, R&D documentation, and proper IP ownership), the company was able to apply for and successfully obtain IDI status for the income generated by these assets. The effective tax rate on income from APAC that qualified for the IDI status was reduced to a concessionary tax rate much lower than the prevailing 17%, while the R&D costs incurred by the Singapore team triggered enhanced deductions that further lowered the amount of tax paid. The lesson: the choices of where IP is developed and owned must be made in advance of the IP development. Hindsight restructuring is expensive and highly scrutinised.

The second case is an example of problems with insufficient valuation documentation. A consumer technology company operating in Australia had a Singapore entity that licensed the group’s software platform to the Singapore entity in return for royalties. The royalty rate was based on an internal estimate, rather than a valuation. On audit, IRAS questioned the royalty rate as being excessive – claiming that it was not at arm’s length and that the tax deductions made artificially lowered the Singapore entity’s taxable income. This resulted in extra tax, interest, and compliance costs. This example highlights the importance of not only understanding how to value intellectual property for tax purposes in SG but also why it is important to manage the risk. Third-party, timely, and well-documented valuations are the main line of defence against transfer pricing adjustments.

A third case is that of an indigenous manufacturing SME that had spent millions of dollars on proprietary process technology over the past 15 years, but had not previously identified or valued its IP. A new CFO with a corporate finance background was hired, and among her first initiatives was an IP audit and valuation. This revealed multiple patentable process innovations, a set of trade secrets that were documented in the company’s operating manuals, and a registered trademark with a high degree of brand value in the local market. With the valuations in hand, the company was able to successfully claim WDA on the cost of acquiring IP that it had formally transferred from the founder to the company, claim enhanced R&D tax deductions on its qualifying research and development expenditure for the first time and commence an application for the Enterprise Development Grant for the development of an IP strategy. The actual tax savings in the first year following the implementation were in the hundreds of thousands of dollars. The takeaway here is that IP tax strategies are not just reserved for tech companies or multinationals; manufacturing, service, and distribution companies often have valuable IP that has never been harnessed for its potential tax advantages.

Challenges in IP Tax Strategy for SG Companies and How to Overcome Them

Although Singapore has a well-rounded IP tax framework, there are common challenges faced by companies, especially SMEs and fast-growing start-ups that are implementing Singapore IP tax incentives for tech startups and other tax incentive strategies. Being aware of these challenges ahead of time minimises the cost of overcoming them.

The most common is the substance test. Singapore IP incentives are not a license to form IP holding companies; they require that there be economic substance (R&D, engineering, product development) in Singapore. Companies operating without this substance that seek to access the IDI or other income-based IP incentives have their applications rejected or income-based IP incentives clawed back on audit. For start-ups with a dispersed workforce across multiple jurisdictions, it can be difficult to meet the Singapore substance test. The key response is to closely document the Singapore activities from the beginning: keep time logs of Singapore employees working on eligible R&D activities, record meeting summaries and technical documents to show that decisions were taken in Singapore, and ensure that contracts in which R&D activities give rise to IP are owned by the Singapore entity.

There is also a second challenge of the interaction between the Singapore tax regime and other countries. An entity with IP held in Singapore that does business with related parties in other jurisdictions must consider not just Singapore tax rules on transfer pricing of the IP, but also withholding tax rules of the source jurisdictions, OECD Base Erosion and Profit Shifting (BEPS) rules, and potentially the domestic anti-avoidance rules of each jurisdiction. This needs to be combined with cross-border tax know-how that many SMEs do not necessarily have. Experience indicates that tax structuring for cross-border IP should be undertaken with advisers who have particular expertise in Singapore and the source jurisdictions – a corporate tax adviser without this expertise is unlikely to see all the issues.

The third issue is timing. The application of many IP tax incentives involves applying for them before the relevant activities start (or the IP is transferred or commercialised). Businesses that only discover the IDI or WDA regime, perhaps because they are raising funds or in discussion for an acquisition, may have missed the opportunity to structure the IP tax incentive. The take-away here is for IP tax planning to be part of the annual finance and strategy review, rather than an “once in a lifetime” review. The IP tax advisers to growth companies in Singapore are increasingly suggesting a formal annual IP review as part of the year-end compliance process, whereby new IP assets are identified, valued, and placed within the incentive structure to maximise efficiency.

Conclusion: Key Lessons on IP Tax Strategy for SG Companies and IP Valuation

Singapore’s IP tax regime is certainly competitive with the rest of the world – but it is not self-serving. They demand careful structuring, meticulous documentation, and a proactive approach to IP identification and valuation, prior to commercialisation. For those looking to build a career in this field, the key skills to acquire are a knowledge of Singapore’s key incentive schemes, familiarity with IP valuation techniques, and an ability to link IP strategy with business structure to meet commercial and regulatory objectives. These skills are in strong demand as the number of Singapore companies in the technology, life sciences, professional services, and advanced manufacturing sectors, understanding the value of their IP assets, continues to grow.

For managers and those engaged with clients, the most practical advice is to advance the IP tax conversation (up the food chain). The most effective way to deal with the tax consequences of IP commercialisation for Singapore SMEs is to deal with it up-front in the creation or purchase of the IP, rather than later in a transaction or audit. Advise clients and colleagues to consider IP valuations and audits as part of annual financial reporting, such as compliance and budgeting. This enables the business to proactively claim incentives, get commercialisation right from the start, and do the transfer pricing work that protects the business.

Finally, stay current. Singapore’s IP tax incentives change with every Budget, and IRAS continues to issue updates for its transfer pricing, R&D, and other IP tax-related regulations. The businesses (and their advisers) that get the most benefit out of it are those who treat it as a dynamic system, rather than a set-and-forget set of rules. Becoming savvy on how to value intellectual property for tax planning in SG, and in all the available incentives, is an investment that pays dividends as you grow your career, and provides tangible value to the companies you advise.